- The Opening Print

- Posts

- Volatility’s Back on the Floor: 100-Point Swings and Zero Mercy Into the Close

Volatility’s Back on the Floor: 100-Point Swings and Zero Mercy Into the Close

Danny Riley

March 31, 2026

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

Today is the last trading day of March and the end of Q1 and the JPM Put or Collar. I would like to say things will be quiet, but I don’t think that's possible. According to Jeff Hirsch's Stock Trader's Almanac, end Q1 is:

• Prone to volatility and weakness since 1990

• March has been taking some mean end-of-quarter hits

• 22 of 36 years since 1990, the last 3–4 trading days of March have been a net loser for the S&P 500

End-of-quarter portfolio restructuring likely plays a role as managers square positions for the next quarter. These declines can begin on either the fourth-to-last trading day or the third.

Market weakness dominated the end of March from 1990 through 2009. From 2010 to 2017, the S&P 500 largely bucked the trend. More recently, late-March selling appears to be staging a comeback, down 5 of the last 8 years.

Historically, end-of-Q1 weakness has occurred regardless of how strong or weak the month had been. In 2009, the S&P was up 13.30% and still declined 4.20% over the last three trading days. The S&P was down 10.97% in 2020 and lost another 1.73% at month’s end. Last year, it was down 2.99% and fell another 2.85% into month end.

With the S & P 500 down 10.31% as of March 30, and absent some resolution with Iran, further declines are likely.

Our Lean — Danny’s Trade (Premium only)

Guest Posts:

Tom Incorvia - Blue Tree Strategies

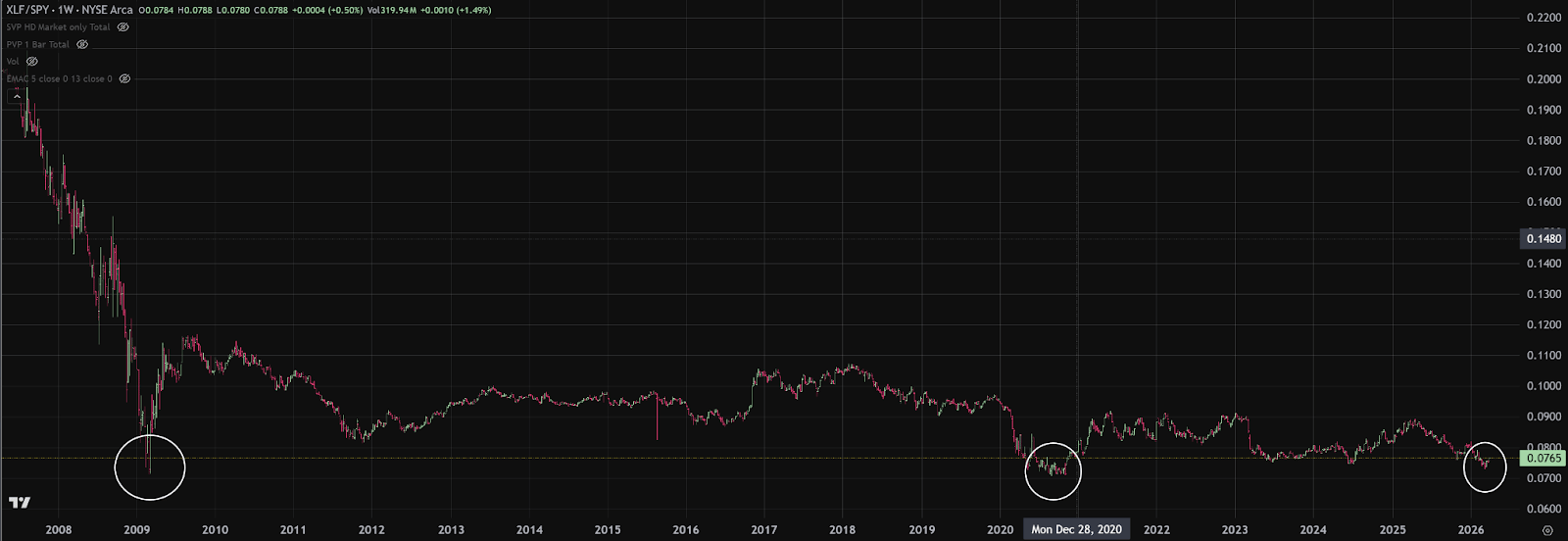

XLF/SPY

The XLF/SPY ratio is approaching a level that has only been seen during periods of significant market stress—most notably the 2008 financial crisis and the 2020 COVID shutdown.

In simple terms, Financials have been underperforming the broader market for an extended period, pushing this ratio down to an area that has historically marked extreme pessimism and potential exhaustion.

While the trend is still clearly lower—and this is not typically the type of environment to step in front of—this level deserves attention. When markets reach these kinds of extremes, the conversation begins to shift from trend continuation to potential inflection.

What matters now is not prediction, but observation.

We want to see:

A slowdown in downside momentum

Signs of relative strength returning to Financials

Evidence that price is beginning to build value, rather than continue lower

Until then, the trend remains intact. But historically, this is where markets begin to transition—if they’re going to.

You can purchase Tom’s Course on Volume Profile here

Rich Miller - [email protected]: HandelStats.com

Last Day of March on a Tuesday: Watch the Reversal Setup

Looking at the last trading day of March since 1980, the broad numbers show a market with no overall bias:

46 occurrences

23 up

23 down

50.0% up

On the surface, that is a completely neutral setup.

But when the last day of March falls on a Tuesday, the data becomes much more interesting.

Last Day of March Falling on a Tuesday

Since 1980, this has occurred 7 times:

5 up

2 down

71.4% positive

That alone is notable, but the more important pattern is what happened the day before.

The Key Tell: Monday Has Been Opposite

In all 7 Tuesday occurrences, the Monday immediately before moved in the opposite direction of Tuesday.

That means:

When Tuesday closed higher, Monday had closed lower

When Tuesday closed lower, Monday had closed higher

So the pattern is not just a Tuesday bias.

It is a reversal relationship from Monday into the final trading day of March when that final day lands on a Tuesday.

Why This Matters

That suggests the market has tended to flip direction from the prior session rather than simply trend through quarter-end.

So the setup to watch is:

Weak Monday → potential strength on Tuesday

Strong Monday → risk of weakness on Tuesday

This turns the study from a simple seasonal stat into something much more useful tactically. It gives traders a conditional framework rather than just a standalone probability.

Bottom Line

Last day of March overall: neutral

Last day of March on Tuesday: bullish bias

Most important detail: the Monday before has been opposite every time

That makes this less of a raw calendar tendency and more of a calendar-based reversal setup.

Headlines, Gamma, and the Trap : @Manny_Trends

We are trading inside a headline-driven minefield.

At the time of writing, futures caught a bid on:

“Progress in US–Iran war talks.”

ES immediately pushed ~20 handles.

That is the tape.

This is exactly the environment we’ve been discussing:

geopolitical tension

energy volatility

policy uncertainty

and now, real-time headline-driven price action

If you’re not careful, this turns into a whipsaw tape quickly.

The Bigger Context

There is still a major macro catalyst hanging over this market:

The Iran situation.

That alone is enough to keep volatility elevated.

I still expect a pump at some point—not because the market is healthy, but because that’s how distribution works.

Markets don’t roll over cleanly.

They reset positioning first.

That requires:

a move higher

a shift in sentiment

a degree of complacency

From a structural standpoint, SPX still has unfinished business in the 6850–6915 range.

But that does not mean we get there cleanly.

What the Book Is Saying

When we were pressing all-time highs, I leaned short—not because of headlines, but because the book suggested distribution.

By “the book,” I mean:

positioning

failed breakouts

expanding ranges

And we saw the result:

~600-point drawdown.

Now?

The book is not signaling clear accumulation.

And in this type of environment, it likely won’t be obvious when it does.

Instead, expect:

failed breakouts

sharp reversals

wide, overlapping ranges

That is distribution behavior.

Gamma Is Driving This Tape

We are in negative gamma.

That changes everything.

In negative gamma environments:

markets expand, not stabilize

hedging amplifies moves, it doesn’t dampen them

Dealers are forced to chase price, which leads to:

larger candles

faster directional moves

exaggerated reactions to headlines

This is why:

breakouts often fail

reversals overshoot

moves feel aggressive and disorderly

The market is not discovering price.

It is reacting to hedging flows.

Bigger Picture Threshold

The market is not structurally bullish yet.

That only begins to change above 6600, where positioning and structure would start to shift more meaningfully.

Until then:

rallies are likely part of the distribution process.

Where the Rubber Meets the Road

This is not a trend environment.

This is a reaction environment:

headlines hit

price moves

gamma expands the move

traders get caught in between

The job is simple:

respect levels

understand the environment

stay flexible

Bias gets punished here.

The Bottom Line

We are in a distribution year.

That likely means:

sharp moves higher

sharp moves lower

and a lot of noise in between

This morning’s headline is the perfect example.

One line of “progress”… and ES moves 20 handles.

That is the tape.

In this environment, edge doesn’t come from predicting.

It comes from reacting faster than positioning can adjust.

If this bigger picture is the map, the daily levels are the execution plan.

I post those each morning on X: @manny_trends

IMPRO members see that work first.

— Manny Payano

Market Recap

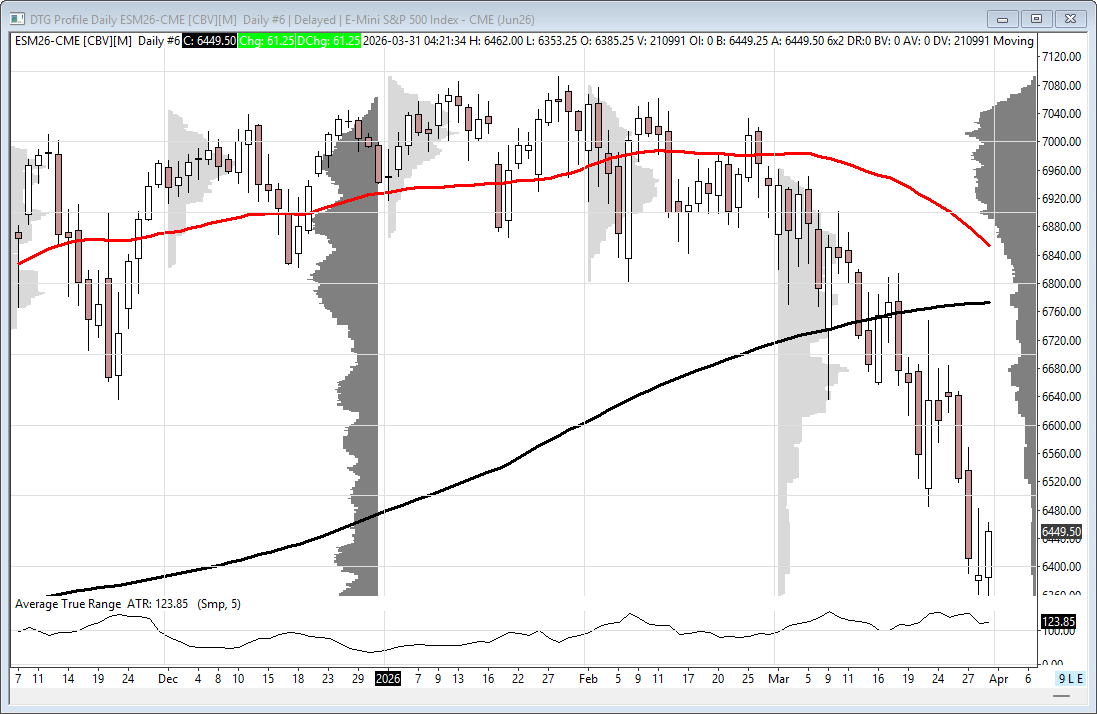

1-Month ESM26 Chart

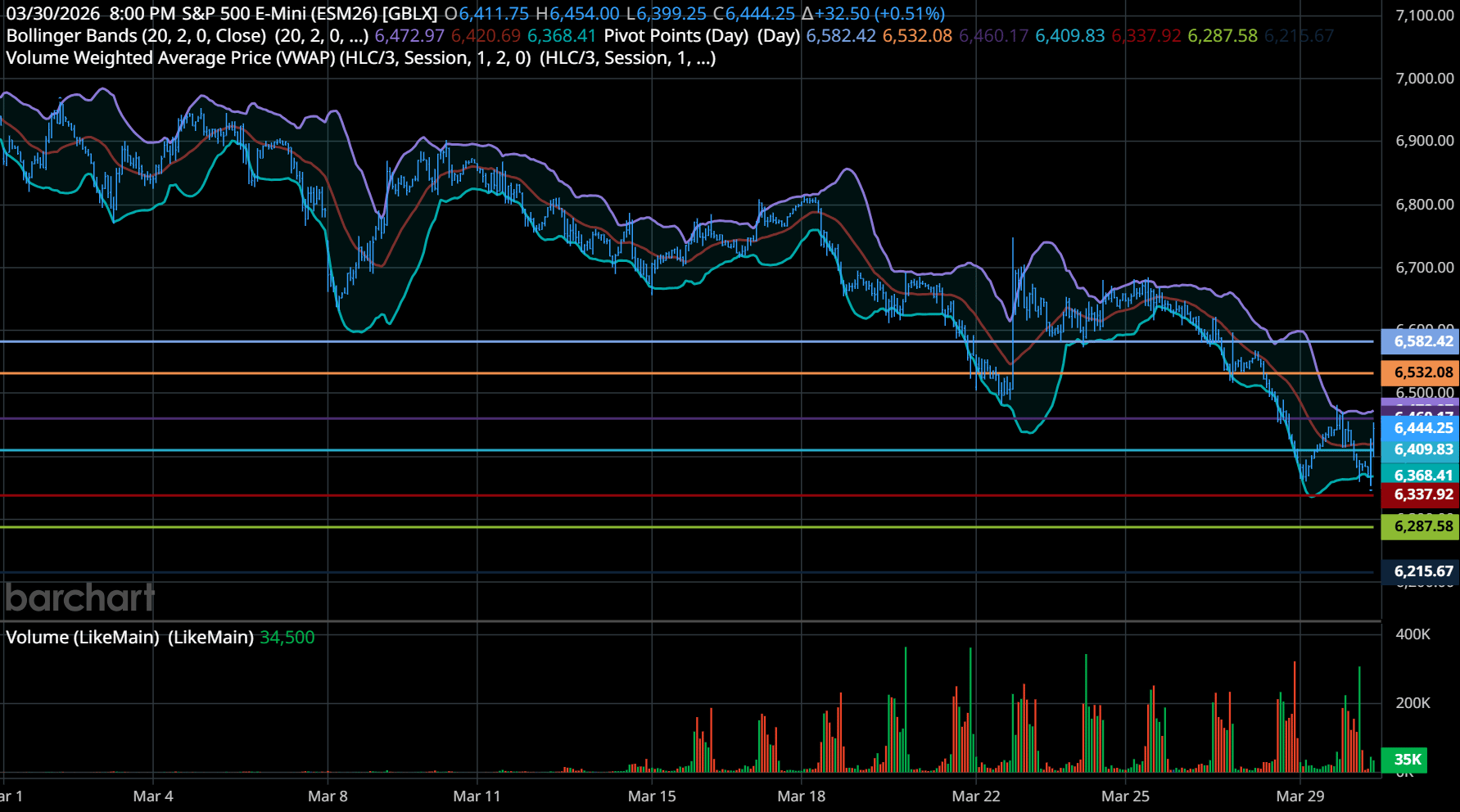

The ES traded 6411.25 and traded up to 6481.75 on Globex, with 380k ES traded, and opened funday Monday's regular session at 6467.75, up 6.50 points.

After the open, the ES traded 6454.75 and rallied up to 6471.25. It then sold off down to 6413.75 at 9:55 and traded up to 6435.50 at 10:10. The ES sold back off to a higher low at 6414.50 at 10:45, then rallied up to a lower high at 6455.75 at 11:05. It sold off down to 6423.00 at 11:15 and rallied up to another lower high at 6452.50 at 11:50. The ES then sold off down to new lows at 6393.75 at 1:35 and rallied up to 6413.50 at 1:45. It sold off down to a new low at 6359.50 at 3:34 and rallied up to 6382.25 at 3:48. The ES traded 6378.00 as the 3:50 cash imbalance showed $280 million to sell, then traded up to 6394.25 at 3:55 and traded 6387.75 on the 4:00 cash close.

After 4:00, the ES traded down to 6377.00, flatlined, and settled at 6388.25, down 24 points or -0.38%, down 3 sessions in a row for a total loss of 252.50 points or -3.84%. The NQ settled at 23139.75, down 188.75 points or 0.81%, also down 3 sessions in a row for a total loss of 1,228 points or -5.12%. The YM settled at 45,465, up 41 points or +0.09%, and the RTY settled at 2428.20, down 35.80 points or 1.45% on the day, or down 3 sessions in a row for a total loss of 123 points or -4.92%.

In the end, we all have to own our own path in life, and we have to make decisions that won't necessarily be easy to make, but the war in the Middle East has added a level of uncertainty and economic stress like we have never seen before. In terms of the ES’s overall tone, it was weak, but I think the real question is... what did you expect? In terms of the ES's overall trade, volume was low at 1.7 million contracts traded.

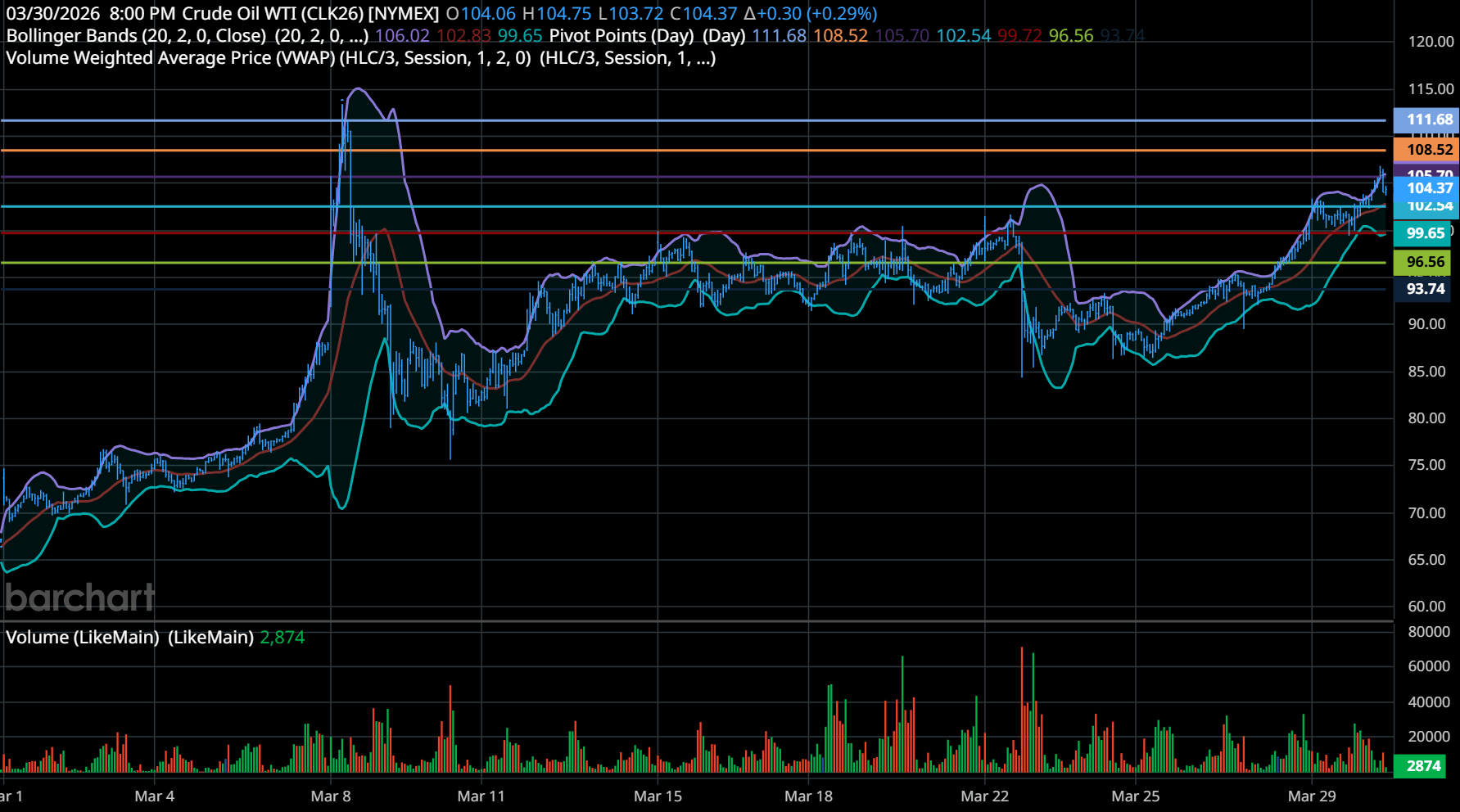

1-Month CLJ26 Chart

Gold rallied, but it's still all eyes on oil. Trump continues with this "talks with Iran are going well," while the US continues to build up its military presence with new ground troops and navy vessels. I get it, the index markets are weak, but the outperformer isn't a stock index or a stock, it’s the $CLK (crude futures), which is currently pricing in more bad news, which has been up 16 of the last 23 sessions, or up $41.81 or +52.25%. Obviously, I can't do the math on my own, so I asked Claud, "At this pace, how long will it take to trade up to 110. 115, 120, 125?" and here is what it said:

Target Price Trading Days Needed Estimated Achievement Date

110.00 ~2.3 Days Thursday, April 2, 2026

115.00 ~5.1 Days Tuesday, April 7, 2026

120.00 ~7.9 Days Friday, April 10, 2026

125.00 ~10.8 Days Wednesday, April 15, 2026

There are many stories of Iran being the big winner due to shutting down the Strait of Hormuz, but how will they export oil with the war going on, and what happens when the war is over? I find it unlikely that energy prices will remain high once oil starts flowing again, but Iran has done billions of dollars in damage to the Middle East oil infrastructure that will take years to rebuild, including rebuilding their own infrastructure, so maybe that is what they are banking on.

On Tap Today

9:00 am: S&P Case-Shiller home price index (20 cities)

9:45 am: Chicago Business Barometer (PMI)

10:00 am: Job openings

10:00 am: Consumer confidence

12:00 pm: Chicago Fed President Austan Goolsbee speaks

3:00 pm: Fed governor Michael Barr speaks

5:10 pm: Fed Vice Chair for Supervision Michelle Bowman speaks

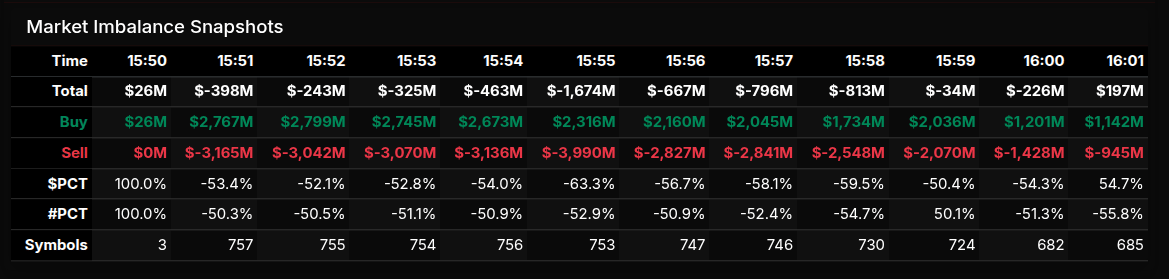

MiM

Market-on-Close Recap – MiM

The MOC session opened with a broadly defensive tone, as early imbalance data at 15:50 showed a modest +$26M buy skew that quickly flipped into sustained sell pressure. By 15:51, the market had sharply transitioned to -$398M, establishing a clear sell-side bias that persisted for most of the auction. The imbalance deepened into the mid-window, reaching a low near -$1.67B at 15:55, marking the session’s peak institutional supply phase. From there, the tape stabilized, with selling pressure gradually moderating into the close, ultimately flipping to a +$197M buy imbalance at 16:01—suggesting late buy programs or rebalancing flows.

Sector behavior reinforced this two-phase structure. Early and mid-session selling was concentrated in Technology (-72.9%), Communication Services (-59.0%), and Healthcare (-60.0%), all of which registered strong directional (non-rotational) sell programs. Technology stood out as the most aggressive, clearly exceeding the -66% threshold, indicating wholesale distribution rather than rotation. Real Estate (-66.3%) also approached this extreme, confirming broad risk-off positioning.

Conversely, buy-side activity was concentrated in Energy (+83.2%), Consumer Defensive (+65.5%), and Financials (+52.9%). Energy was particularly notable, exceeding the +66% threshold and signaling aggressive accumulation. Consumer Cyclical (+60.7%) and Utilities (+54.2%) leaned positive but remained more rotational in nature.

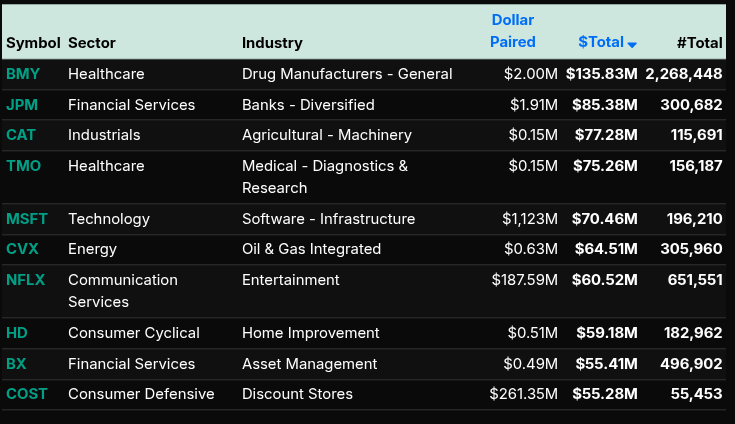

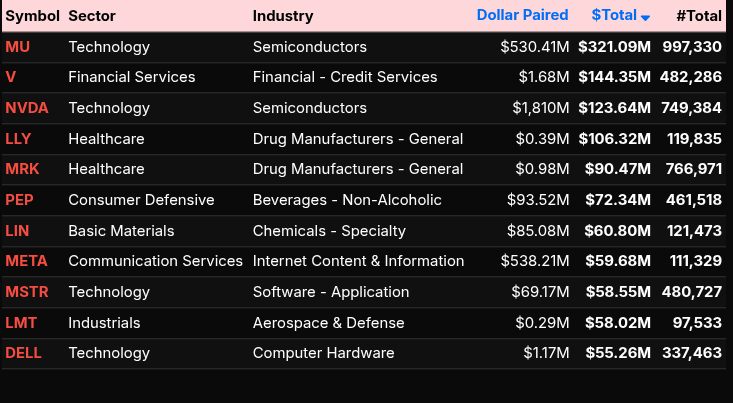

On the single-name level, the sell pressure was led by large-cap tech: NVDA, META, MSFT, and MSTR all contributed to the imbalance, reinforcing the sector-wide liquidation theme. Communication weakness via META and NFLX further confirmed growth-oriented outflows. On the buy side, flows rotated into defensives and cyclically stable names such as BMY, JPM, CVX, and COST. Notably, MU printed the largest paired volume but still closed as a net buy, reflecting two-way institutional activity rather than outright conviction.

Overall, the session evolved from broad sell-side pressure into a late buy imbalance, with clear sector rotation out of high-beta tech and into energy and defensive positioning.

Technical Edge

Fair Values for March 31, 2026:

SP: 43.04

NQ: 182.53

Dow: 236.13

Daily Market Recap 📊

For Monday, March 30, 2026

• NYSE Breadth: 46% Upside Volume

• Nasdaq Breadth: 44% Upside Volume

• Total Breadth: 45% Upside Volume

• NYSE Advance/Decline: 50% Advance

• Nasdaq Advance/Decline: 42% Advance

• Total Advance/Decline: 45% Advance

• NYSE New Highs/New Lows: 90 / 168

• Nasdaq New Highs/New Lows: 60 / 537

• NYSE TRIN: 1.10

• Nasdaq TRIN: 0.90

Weekly Breadth Data 📈

For Week Ending Friday, March 27, 2026

• NYSE Breadth: 54% Upside Volume

• Nasdaq Breadth: 46% Upside Volume

• Total Breadth: 49% Upside Volume

• NYSE Advance/Decline: 47% Advance

• Nasdaq Advance/Decline: 39% Advance

• Total Advance/Decline: 42% Advance

• NYSE New Highs/New Lows: 156 / 308

• Nasdaq New Highs/New Lows: 217 / 837

• NYSE TRIN: 0.74

• Nasdaq TRIN: 0.72

ES & NQ Levels (Premium only)

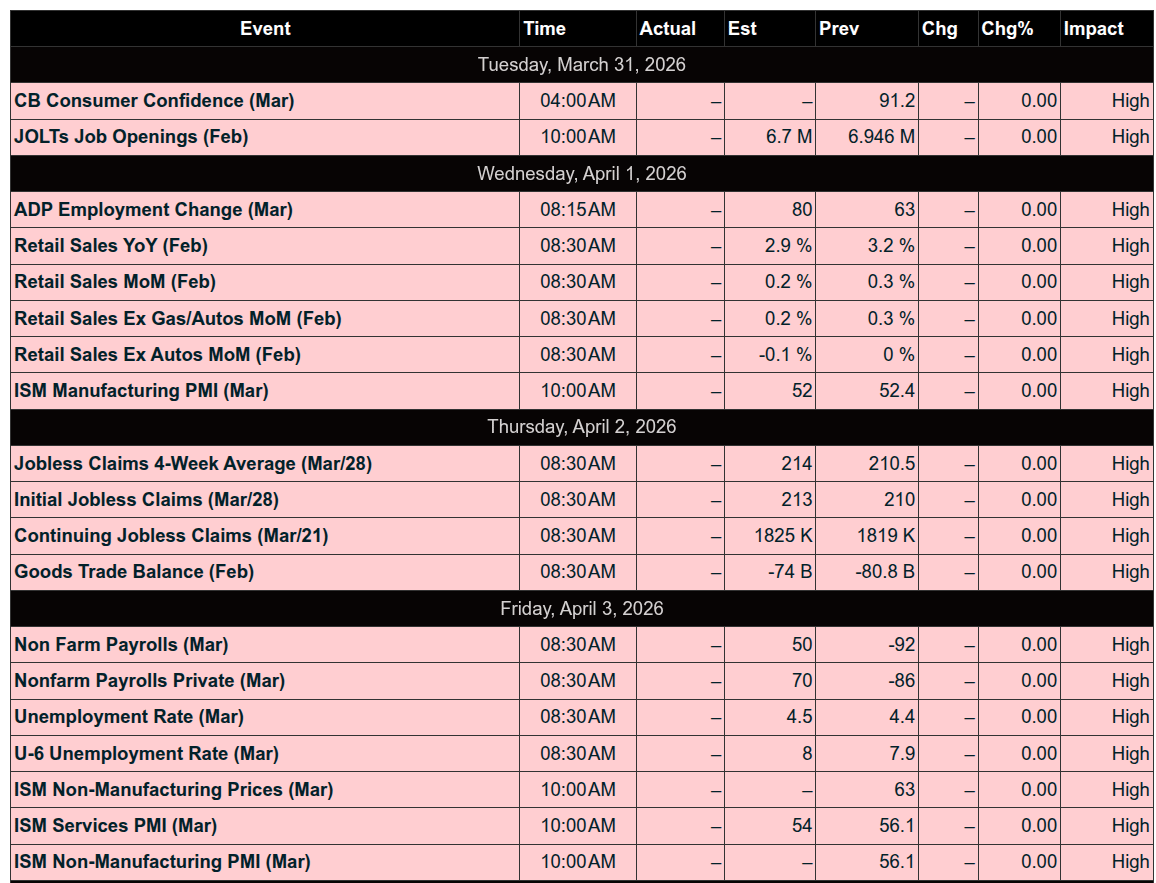

Calendars

Economic Calendar

Trading Room Summaries

Polaris Trading Group Summary - Monday, March 30, 2026

Monday was a highly directional, trend-driven downside day, with excellent read-through from David on structure, cycle projections, and key levels. The room capitalized well on both early opportunities and sustained downside continuation.

Market Narrative

Overnight, ES tagged the 6365 D-Level and reversed sharply, setting the stage for early positioning.

Price pushed higher into the open, but David identified this as a classic “Jam n Slam” setup:

Weak structure from overnight ramp

Lack of real buyers underneath

This led to a clean transition from early strength → sustained sell pressure

Key Trades & Wins

1. Crude Oil (CL) – Clean Open Range Winner

Open Range Long hit target quickly

Follow-through confirmed strength above the “hundo” marker

Later: All long OR targets fulfilled

Great example of letting the OR setup play out cleanly without overthinking

2. ES / NQ – Open Range Shorts

Early recognition of weak structure despite initial push up

Open Range Shorts triggered and hit initial targets

NQ noted as weaker than ES, reinforcing short bias

Strong read on relative weakness + structure = high-probability short

3. Trend Day Down – Cycle Alignment

Price “bled red from the open” with little meaningful bounce

Key downside levels were systematically called and hit:

6405.98 (cycle projection)

6389 (Prior Low)

6381.49 – 6378.30 zone

6369 → 6364 zone

This was a textbook level-to-level trend day, rewarding patience and holding runners.

4. D-Level Reaction (Late Day)

Late session bounce off D-Level produced ~20+ point reaction

Led to reclaim of Prior Low (6389) into the close

Reinforces the importance of:

Trusting key structural levels

Staying engaged even late in the session

Key Lessons & Insights

1. “Jam n Slam” = Sell the Weak Structure

Overnight strength ≠ real strength

When structure is poor, expect air pockets on pullbacks

Buyers were “non-existent” → strong conviction to short

2. Follow the Levels, Not Emotion

The day was a perfect example of disciplined level trading

Each downside target was:

Predefined

Hit in sequence

No guessing, just execution

3. Not Every Signal is a Trade

Midday 200XT setup was identified but passed due to poor structure

Critical reminder: Clean configuration > forcing trades

4. Cycle Awareness Matters

Market hit Cycle Day projections early

Discussion of a potential failed 3-day cycle (rare event)

Adds context to:

Why downside extended

Why bounces were weak

5. Patience Pays on Trend Days

Many opportunities, but the biggest gains came from:

Holding shorts

Trusting continuation

As one member noted: “Your short is printing wow”

Final Takeaway

This was a model PTG trend day:

Identify weak structure early

Execute OR setups

Trust downside levels

Stay patient for continuation

The biggest edge came from alignment of structure + cycles + levels

Discovery Trading Group Room Preview – Tuesday, March 31, 2026

Market Brief – Morning Update

Macro Focus: Middle East conflict remains the primary driver

Sentiment Boost: WSJ report of potential US–Iran negotiations lifted futures

Oil: Holding >$100 → near-term inflation pressure

Fed Takeaways:

Williams: Oil likely to push inflation higher short-term

Powell:

Rates “in a good place” → wait-and-see mode

No signs of systemic risk / contagion

Tariff-driven inflation seen as temporary

Geopolitics:

إيران attack on oil tanker near Dubai (no casualties, no leak)

Continued missile/drone escalation across Gulf, Israel, Turkey

Rising risk premium in energy markets

Market Risks:

Sustained high oil →

ضغط on consumers & corporate margins

Potential pullback in AI/data center capex

Broader equity market correction risk

Today’s Catalysts:

9:00 ET: HPI

9:45 ET: Chicago PMI

10:00 ET: JOLTS + Consumer Confidence (key)

Fed speakers throughout day

Earnings: MKC, SNX (pre) | NKE (post)

Flows & Volatility:

Volatility: Still elevated (ADR ~123.5, down ~30 pts)

Whale flow: Slight bullish lean, lighter volume

ES Technicals:

Holding downtrend channel support: 6344/39

Breakdown below → 6135 major support

Resistance ladder:

6609/04

6712/07

6900/95

50DMA (6852) accelerating toward 200DMA (6772)

Bottom Line:

Near-term: Bulls have room above channel support

Bigger picture: Oil + geopolitics remain the key risk drivers