- The Opening Print

- Posts

- Snowed in. Blizzard of 2026

Snowed in. Blizzard of 2026

Danny Riley

February 23, 2026

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

There Is A Storm Brewing Out There

A blizzard warning has been issued for New York City, Long Island, and parts of New Jersey, Connecticut, Massachusetts, and Maine. Snowfall totals of 12–24 inches are expected, with some areas locally seeing up to 2 feet. Snowfall rates could reach 1–3 inches per hour, along with wind gusts of 50–60+ mph, causing whiteout conditions.

The heaviest snow is expected Sunday night into Monday morning. Mayor Zohran Mamdani has issued a travel ban from 9 pm Sunday to noon Monday and closed schools on Monday. Governor Kathy Hochul has declared a state of emergency and activated the National Guard.

Expect major travel disruptions and possible power outages. Stay home and monitor the National Weather Service and New York City Emergency Management for updates.

Our View

It’s going to be another week of shake, rattle, and roll. Between the blizzard heading to the East Coast, economic reports, Fed speak, earnings, Treasury auctions, and NVDA on Wednesday, there’s a lot on the table.

Is the S&P going up this week? There are so many unpredictable factors like news flow, geopolitics, and surprises in data and earnings. But based on some analyst views and forecasts, it sounds like the near-term leans are cautiously mixed to slightly bullish, with continued elevated volatility.

Our Lean

Market Recap

The ES traded up to 6904.75, sold off down to 6847.50 and traded 6852.75, down 25.5 points or -0.37%. We knew this was going to be a volatile day, and it didn’t let down, as Q4 2025 GDP slowed to 1.4% (missing the 2.5% forecast), largely due to the government shutdown. Simultaneously, inflation proved sticky, with Core PCE rising to 3.0% YoY. This combination of stagnant growth and hot prices likely forces the Fed to remain hawkish, keeping near-term rate cuts off the table.

After the open, the ES sold off down to 6847.25, rallied up to 6884.00 at 9:40, pulled back to 6864.00, and then rallied up to 6925.00 at 10:00 after the US Supreme Court struck down President Donald Trump’s sweeping global tariffs imposed under the International Emergency Economic Powers Act (IEEPA) of 1977. In a 6-3 decision authored by Chief Justice John Roberts (joined by Justices Barrett, Gorsuch, and the three liberal justices), the Court held that IEEPA does not authorize the President to unilaterally impose tariffs, as this would intrude on Congress’s constitutional authority over taxation and commerce.

After the rip, the ES sold off down to 6872.200. It then rallied up to a lower high at 6923.50 at 11:00. The ES sold off down to a higher low at 6889.25 at 11:30 and rallied up to another lower high at 6922.75. It then sold off down to 6871.00 at 12:25 and rallied back up to 6909.00 at 1:05, just before Trump went live (always late). The ES sold off down to 6887.25 at 1:15 and rallied up to 6931.00 at 1:43. It then sold off down to 6908.75 at 2:49 (slow walk selling).

The ES rallied up to 6924.25 at 3:09, then sold back off down to 6912.00 at 3:22. It rallied 10 points and traded 6918.00 as the 3:50 cash imbalance showed $1.4 billion to buy, traded up to 6926.25, and traded 6924.75 on the 4:00 cash close.

After 4:00, the ES traded up to 6929.25 at 4:05 and settled at 6923.25, up 46.25 points or +0.67%. The NQ settled at 25,067.50, up 208.75 points or +0.84%, the YM settled at 49,647, up 216 points or +2.16%, and the RTY settled at 2,641.10, down 0.30 point or 0.01% on the day.

In the end, the market giveth and the market taketh it away. In terms of the ES and NQ’s overall tone, the down open was a big buy op. In terms of the ES’s overall trade, volume was higher at 1.739 million contracts traded.

It doesn’t really matter what the cause of Friday’s rally was, but the ES rallied 87 points off its 6847.25 low and closed above the big figure of 6900.00, the first close above this level in 7 sessions. Was it the economic numbers? I think not. Was it the gap down and everyone being too short? I think that was part of it, but I think the main driver was the options expiration and the short gamma positions.

This Week’s Major U.S. Economic Reports & Fed Speakers

Mon Feb 23

08:00 Waller (Fed)

10:00 Factory Orders

Tue Feb 24

08:00 Goolsbee (Fed)

09:00 Case-Shiller | Bostic (Fed)

09:15 Waller (Fed)

09:30 Cook (Fed)

10:00 Wholesale Inventories + Consumer Confidence

Home Depot (HD) earnings

2Y Note auction ($69B)

Wed Feb 25

Before open: Lowe’s (LOW)

09:35 Barkin (Fed)

11:00 Schmid (Fed)

5Y Note auction ($70B)

After close: Nvidia (NVDA), Salesforce (CRM)

Thu Feb 26

08:30 Jobless Claims

Fri Feb 27

08:30 PPI + Core PPI

09:45 Chicago PMI

10:00 Construction Spending

MiM

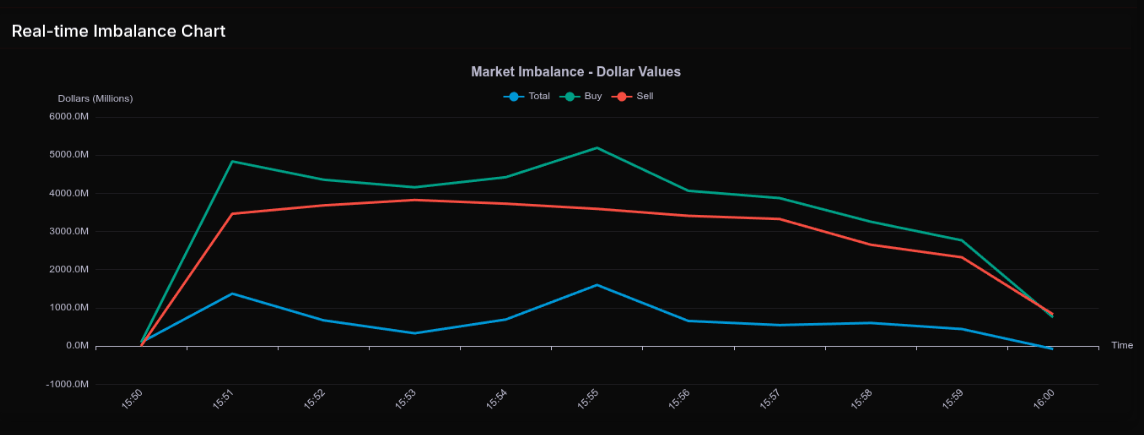

The February 20th MOC session opened with a firm bid and built steadily into the 15:55 snapshot before fading sharply into the 16:00 print. At 15:50, the market showed a modest $94M buy imbalance, but by 15:51 that expanded aggressively to $1.37B net buy, driven by $4.83B of buy orders versus $3.46B for sale. From there, the tape rotated but held a constructive tone, peaking at 15:55 with $1.59B to buy. Into the close, however, buy pressure evaporated and the final snapshot flipped to a $78M sell imbalance, with -52.5% dollar lean, reflecting a late offset.

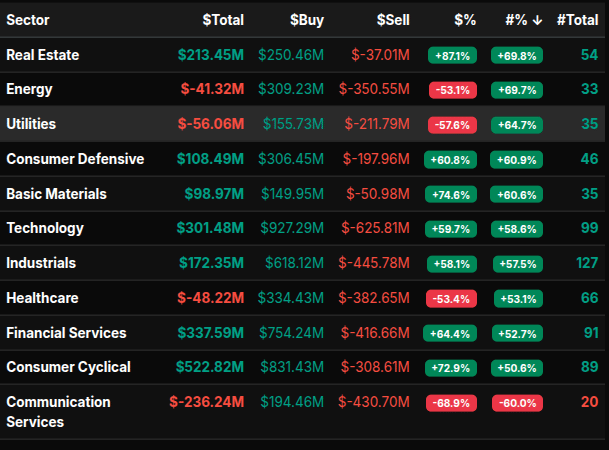

Sector flows were broadly constructive. Real Estate led with an +87.1% lean, indicating a wholesale-style buy program. Basic Materials (+74.6%) and Consumer Cyclical (+72.9%) also showed strong institutional demand. Communication Services stood out on the sell side at -68.9%, a notable wholesale sell imbalance. Energy (-53.1%), Utilities (-57.6%), and Healthcare (-53.4%) reflected more rotational selling pressure rather than outright liquidation, given their proximity to the 50% threshold.

Technology posted $301M to buy with a +59.7% lean, firmly positive but rotational. Financials were similar at +64.4%, while Industrials printed +58.1%. The strongest index-level pressure came from Nasdaq, which leaned +65.4%, just shy of the 66% wholesale threshold, suggesting aggressive growth buying into the bell.

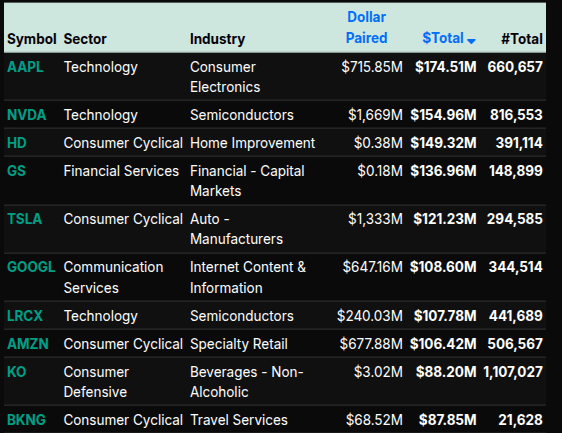

On the symbol level, the largest buy imbalances included MSFT ($206M), AAPL ($174M), NVDA ($155M), and GS ($137M). Consumer names like HD ($149M), TSLA ($121M), and AMZN ($106M) reinforced the cyclical bid. On the sell side, GOOG showed a sizable paired imbalance but net selling pressure, while energy heavyweights XOM and CVX also saw distribution.

Overall, the MOC reflected broad-based accumulation across cyclicals and tech, partially offset by targeted selling in Communication Services and defensive areas, before a late imbalance flip into the closing print.

Technical Edge

Fair Values for February 23, 2026

SP: 12.42

NQ: 53.38

Dow: 38.42

Daily Breadth Data 📊

For Friday, February 20, 2026

• NYSE Breadth: 61% Upside Volume

• Nasdaq Breadth: 53% Upside Volume

• Total Breadth: 54% Upside Volume

• NYSE Advance/Decline: 60% Advance

• Nasdaq Advance/Decline: 53% Advance

• Total Advance/Decline: 55% Advance

• NYSE New Highs/New Lows: 168 / 50

• Nasdaq New Highs/New Lows: 199 / 176

• NYSE TRIN: 0.94

• Nasdaq TRIN: 1.01

Weekly Breadth Data 📈

For Week Ending February 20, 2026

• NYSE Breadth: 55% Upside Volume

• Nasdaq Breadth: 56% Upside Volume

• Total Breadth: 55% Upside Volume

• NYSE Advance/Decline: 59% Advance

• Nasdaq Advance/Decline: 56% Advance

• Total Advance/Decline: 57% Advance

• NYSE New Highs/New Lows: 404 / 116

• Nasdaq New Highs/New Lows: 407 / 492

• NYSE TRIN: 1.19

• Nasdaq TRIN: 1.00

BTS Levels - (Premium Only)

Calendars

Today’s Economic Calendar

This Week’s Important Economic Events

Upcoming Earnings - SP500

Recent Earnings

Room Summaries:

Polaris Trading Group Summary - Friday, February 20, 2026

“FRYDay” – Discipline Pays

The day began with David posting the Daily Trade Strategy (DTS) and key links, setting the tone for a structured and rule-based session. Early on, we saw strength in the plan as the BEAR CASE target at 6860 was fulfilled, confirming alignment with the projected downside objective right out of the gate.

Morning Session – Volatility Meets Discipline

Mid-morning brought unexpected news:

Breaking headline – Supreme Court strikes down Trump tariffs.

This injected volatility into the market, and David reinforced a key lesson:

“Normal ‘game-play’ regardless of SCOTUS decision – Follow your plan.”

That reminder was critical. News can create emotional reactions, but PTG methodology is built to handle volatility through structure, not impulse.

Major Wins – Strategy Execution

Open Range Strategy TRIFECTA!

David posted confirmation of a full Open Range Strategy trifecta — a high-probability, rule-based setup that delivered cleanly. This was a standout achievement of the session.

Later in the morning:

Cycle Day 1 Low Projection – Fulfilled

Cycle Day 1 High Range Projection – Fulfilled

Both sides of the projected range were achieved — a powerful demonstration of:

The accuracy of the 3-Day Cycle framework

Respect for structured projections

The market’s tendency to complete its measured objectives

David emphasized:

“Power of the 3 Day Cycle.”

This was a textbook example of how cycle projections frame the day’s expectations and allow traders to anticipate both extremes rather than react emotionally.

Key Lessons from the Day

Follow the Plan – Especially During News

The Supreme Court ruling created volatility, but the strategy remained the anchor. Discipline over headlines.Cycle Projections Provide Structure

When both high and low projections are fulfilled, it reinforces confidence in trusting the model rather than guessing.Open Range Strategy Continues to Deliver

The trifecta underscores the importance of mastering the opening framework — it often sets up the best opportunities of the session.Community & Process Matter

Traders asked about stops, entries (A10, A4), and mechanics — reinforcing that clarity in execution is just as important as the setup itself.

DTG Room Preview – Monday, February 23, 2026

Macro Focus

Market centered on US tariff uncertainty and upcoming US-Iran talks.

Supreme Court ruled Trump’s most sweeping tariffs illegal → initial bullish reaction Friday.

Trump followed with announcement raising baseline import tariffs from 10% to 15%, effective immediately.

Justification: Section 122 (Trade Act of 1974) citing a balance-of-payments crisis.

Economists largely dispute existence of such a crisis → legal challenges likely.

Bessent: Section 122 seen as a 5-month “bridge” while 232/301 investigations are conducted.

US Customs has halted collection of tariffs ruled illegal.

EU rejects any further US tariff increases, wants adherence to prior trade deal.

China reviewing ruling, calling for removal of unilateral tariff measures.

Geopolitics

US-Iran nuclear talks resume Thursday (Feb 26) in Geneva.

US increasing regional military presence.

Iran signaling openness to diplomacy but rejecting pressure tactics.

Earnings

Premarket: D

After close: OVV, OKE, KEYS, CIB, FANG

Tuesday AM: HD, AS, AMT, BNS, CEG, DDS, ELAN, FIS, FMS, KDP, NRG, VIV

Economic Calendar

8:30am ET – Fed Gov. Waller

10:00am ET – Factory Orders (delayed release)

Volatility / Flow

Friday: 40-point range on SCOTUS headline.

ES 5-day ADR: 82 handles (moderately elevated).

No whale bias overnight – large trader volume light.

Technical Backdrop (ES)

3-month sideways consolidation under ATHs.

Trading near midpoint of short-term downtrend channel.

Still inside intermediate-term uptrend channel.

50-day MA (6933) capped Friday’s HOD → near-term resistance.

Both sides have room within current structure.

Potential TL Levels

Resistance: 6985/82s, 7160/65s

Support: 6810/13s, 6677/72s

Bottom Line

Macro headline risk elevated (trade + Iran).

Range conditions remain intact.

Expect two-sided trade within established consolidation unless new policy headlines shift momentum.