- The Opening Print

- Posts

- Oil Reserves or Not, This War’s Got the Energy Pit Jumpin’ Like It’s ’87

Oil Reserves or Not, This War’s Got the Energy Pit Jumpin’ Like It’s ’87

Follow @MrTopStep on Twitter and please share if you find our work valuable!

FREE Two-Week Offer for the Opening Print Premium. Open up the Lean and other premium features for the next Two Weeks!

Our View

Iran is not giving up, and I don’t think it will. The conflict will continue to overshadow the global market until the attacks stop.

The International Energy Agency (IEA) has proposed the largest release of oil reserves in its history to bring down crude prices that have soared amid the U.S.-Israel war with Iran. France's finance minister said the Group of Seven advanced economies was prepared to release strategic oil reserves to stabilize the global energy market if necessary.

The remarks came after an extraordinary meeting of the group and as Gulf oil producers cut production amid shipping disruptions in the Strait of Hormuz. The Saudi Aramco chief executive cautioned of “catastrophic consequences for oil markets” the longer the disruption to energy flows continues.

Releasing oil reserves may lower oil prices, but I think it will be temporary.

Our Lean — Danny’s Trade (Premium only)

NOTE DATE CHANGE #####

Market Recap

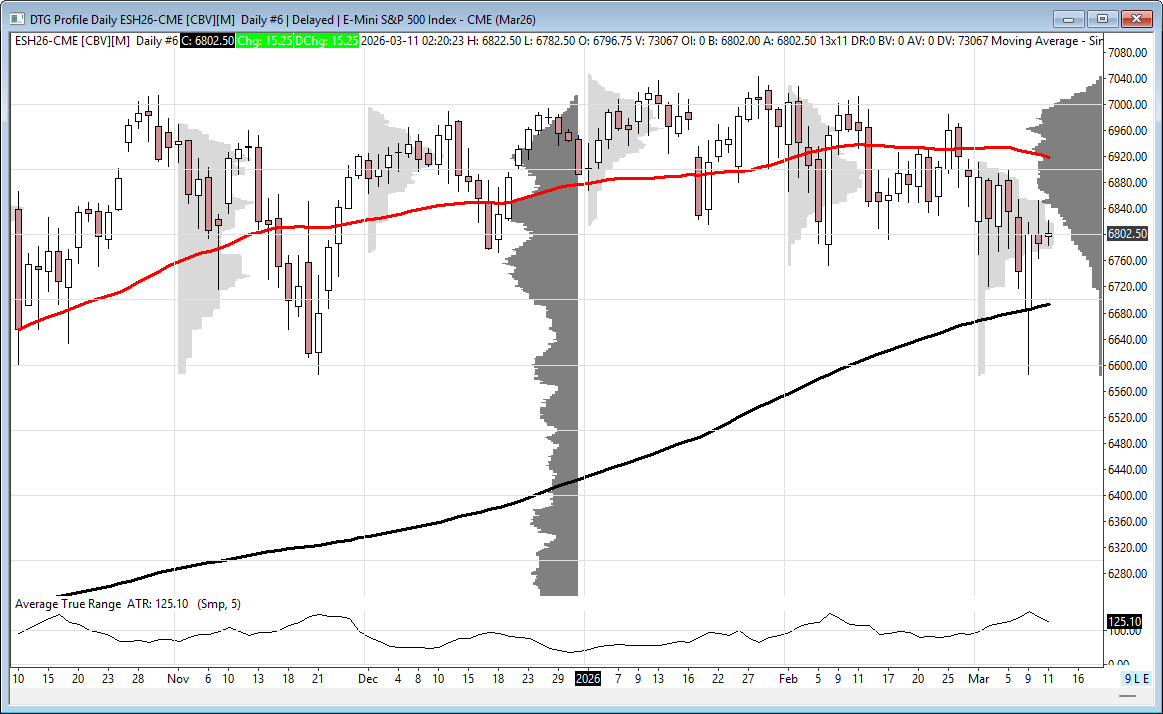

The ES traded down 6762.50 and back up to the resistance at 6833.50 on a bit less volume, with Globex volume of only 520k, and opened Tuesday’s regular session at 6795.00, down 6.75 points or -0.10%.

After the open, the ES traded 6789.25, shot up to 6806.00, then sold off down to 6765.00 at 10:05 and fell into buy program mode. It rallied up to 6835.00 at 11:00, pulled back to 6820.00, and then rallied up to a new high at 6837.50 at 11:40.

The ES then sold off down to 6814.50 at 12:05, rallied up to 6852.25 at 1:35, and quickly sold off down to 6824.50 at 1:39. It rallied up to 6844.00 at 1:50, sold off down to 6791.25 at 2:20, and rallied up to a lower high at 6821.50.

The ES then sold off down to 6782.00 at 3:45 and traded 6785.25 as the 3:50 cash imbalance showed 1.1B. It traded up to 6789.75, sold back off down to 6779.50 at 3:55, and traded 6788.00 on the 4:00 cash close.

After 4:00, the ES traded 6801.50 at 4:10, sold off down to 6795.00, and settled at 6787.25, down 13.75 points or -0.20%. The NQ settled at 24,982.50, down 8.50 points or -0.03%, the YM settled at 47,745, down 24 points or -0.05%, and the RTY settled at 2550.50, down 3.40 points or 0.13% on the day.

In the end, the trade was up, down, and all around. In terms of the ES’s and NQ’s overall tone, they shook off the early sell-off and spent a good portion of the day going up, but when the headlines about Iran striking Abu Dhabi's fuel storage hit, crude rallied and the index markets sold off. In terms of the ES’s overall trade, volume was lower at 1.84 million contracts traded.

Unintended Consequences

While the ES has been down 6 out of the last 7 sessions, it doesn't seem like that is the main focus. Clearly, the markets are more focused on the energy markets, specifically crude oil and reports from U.S. intelligence indicating Iran has begun laying naval mines in the Strait of Hormuz, effectively halting or severely disrupting shipping through the strait, and the threat of U.S. Navy escorts.

Crude oil futures (CLJ26) rallied up to 119.48 Sunday night and fell to 76.73 yesterday, down 42.75 from it's previous level until the headlines hit the tape that the largest oil refinery in the Middle East, located in the United Arab Emirates, was hit by Iranian drones around 12:30 ET, pushing the future up to the $88.00 area just after 2:30.

Iran's attacks on oil production and shipping are going to be the focal point of the markets until there is a resolution.

BREAKING: UAE's Abu Dhabi confirms an Iranian drone hit the Ruwais Industrial Complex. Authorities are battling a fire at the scene but report no injuries. Ruwais is the Middle East's largest refinery complex.

On Tap Today

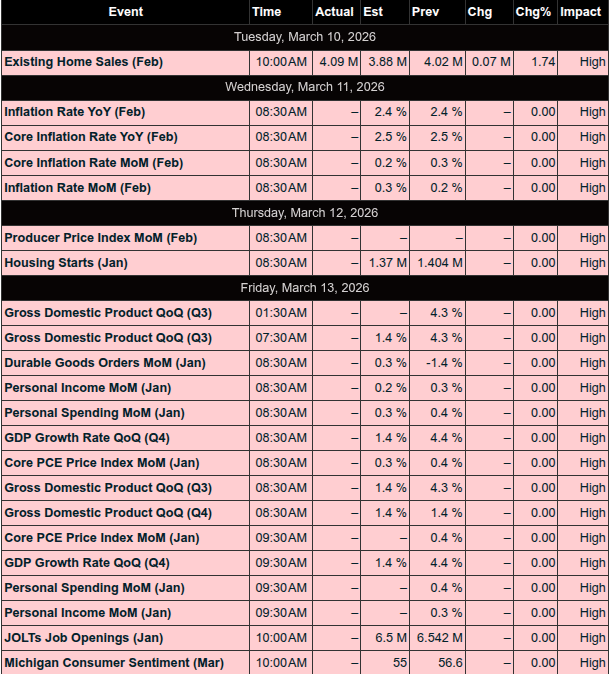

8:30 am: Consumer Price Index (Feb)

2:00 pm: Monthly U.S. Federal Budget (Feb)

Guest Posts

Polaris Trading Group

Transition: Cycle Day 1 → Cycle Day 2

“The Only Easy Day Was Yesterday”

Cycle Day 1 was the gift.

The market did what it was supposed to do — emotional relief, mechanical responses, opportunistic entries for traders who were patient enough to wait for the decline and disciplined enough to act.

Now that gift is gone.

Cycle Day 2 doesn’t reward hope. It rewards execution.

Just like the SEALs’ mantra, the lesson is simple:

Yesterday's difficulty is today’s baseline — not today’s challenge.

Cycle Day 2 Mindset

Expect harder trade location

Expect faster punishment for mistakes

Expect fewer, higher-quality opportunities

Demand better execution than yesterday

This is where traders either:

Lean on process

Or get exposed by emotion

Cycle Day 1 rewarded those who waited and executed at the correct time.

Cycle Day 2 rewards those who stay sharp after being right.

Because in markets — just like in elite training —

The only easy day was yesterday.

🎯 Cycle Day 2 — Scenarios in Play

🟢 Bull Case — Buyers Stay in Control

Acceptance north of 6800 ±5

Upside objectives:

• 6840

• 6830

• 6820

Momentum remains constructive as long as price holds above the pivot zone.

🔴 Bear Case — Rotation / Reset

Acceptance south of 6800 ±5

Downside objectives:

• 6780

• 6770

• 6760

Failure to reclaim the pivot opens the door for a controlled reset, not panic.

📊 Key Reference Levels

• PVA High Edge: 6830

• PVA Low Edge: 6780

• Prior POC: 6788

— PTG

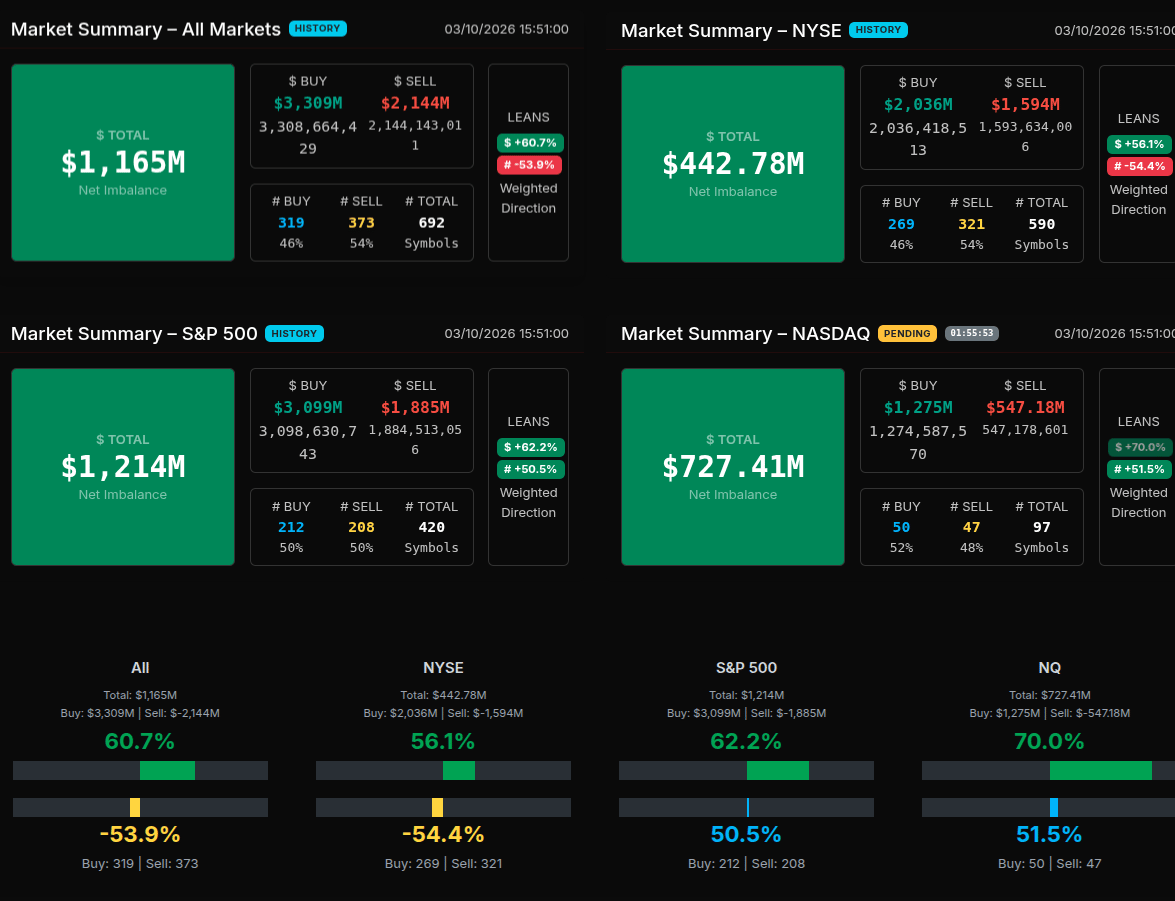

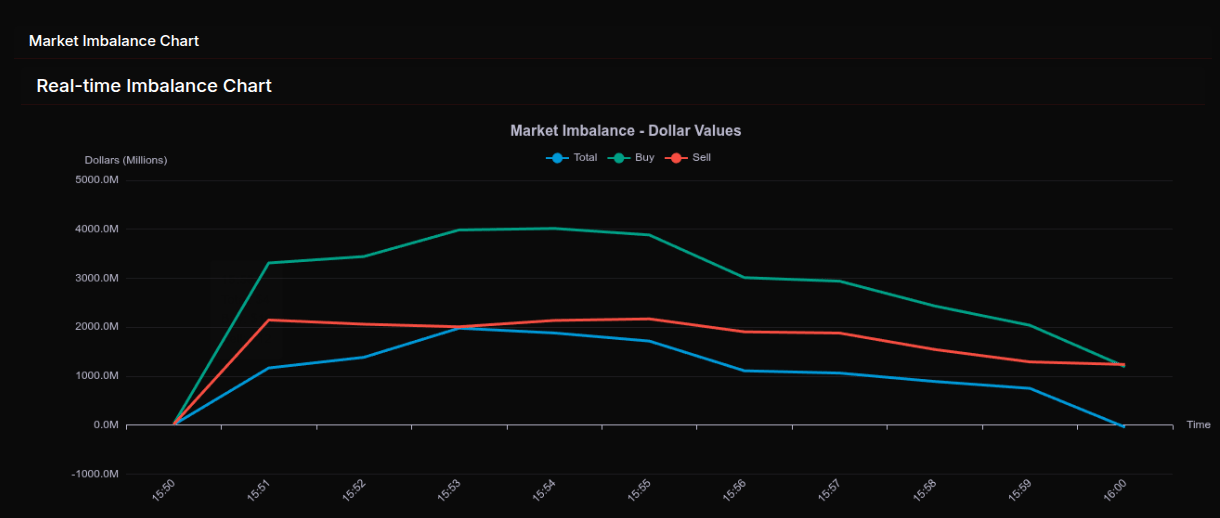

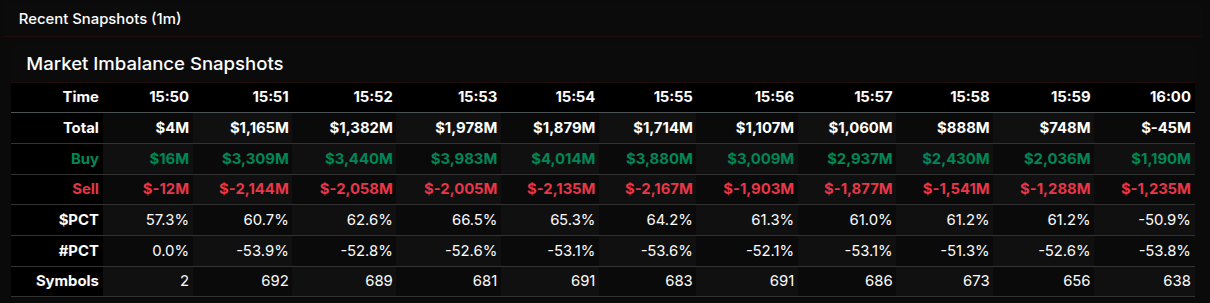

MOC Recap

The closing auction on March 10 developed with a clear buy-side bias early in the imbalance window before gradually rotating into a more balanced finish. At 15:50, the market opened with a modest $4M net buy imbalance, but the tone quickly strengthened as buy interest surged. By 15:51, the imbalance expanded sharply to $1.165B with buy orders reaching $3.3B against $2.14B in sells, setting the stage for a buy-leaning close. The imbalance continued to build into 15:53 where it peaked near $1.98B as buy orders approached $4B. During this phase the percentage lean reached roughly 66.5%, signaling a strong directional institutional bid rather than simple rotation.

After that peak, the imbalance began to steadily contract. From 15:55 onward both buy and sell liquidity declined, with buy interest fading faster than earlier in the window. The total imbalance compressed from $1.7B to under $750M by 15:59 before flipping slightly negative into the close at –$45M. This late shift suggests closing cross participation absorbed most of the earlier demand, leaving the auction balanced at the final print.

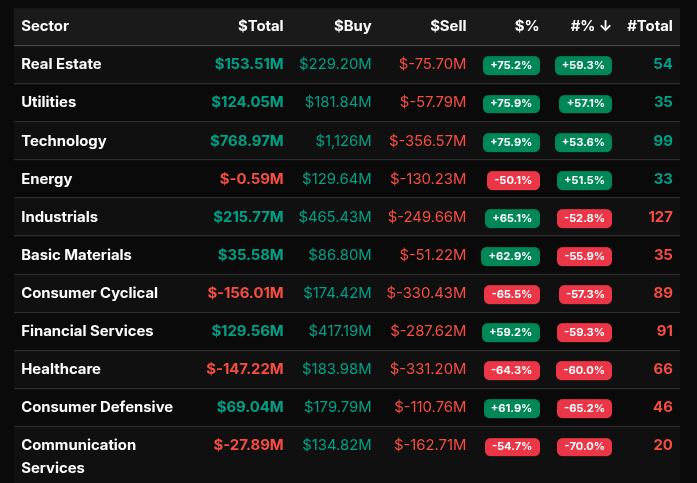

Sector activity revealed where the strongest institutional flows were concentrated. Technology dominated the tape with $768.97M in net imbalance and a 75.9% buy lean, reflecting broad accumulation across large-cap software and semiconductor names. Utilities and Real Estate also showed aggressive buying with 75%+ lean readings, levels that indicate wholesale market-on-close buying rather than rotation. Industrials posted $215M of net demand with a 65% buy lean, just below the wholesale threshold but still reflecting strong institutional participation.

Conversely, several sectors showed distribution. Consumer Cyclical (–65.5%), Healthcare (–64.3%), and Communication Services (–54.7%) leaned toward selling pressure, although these readings were closer to rotational flows rather than outright liquidation.

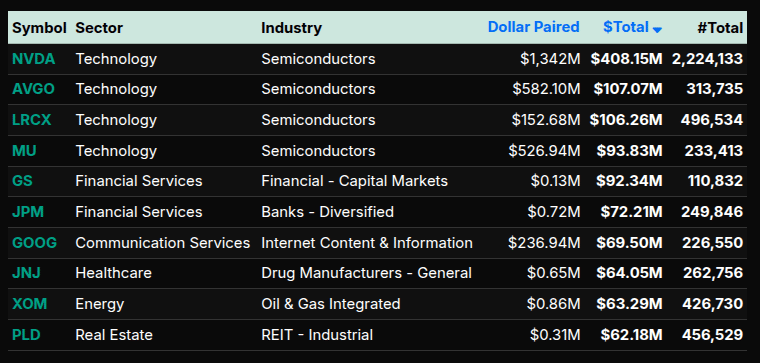

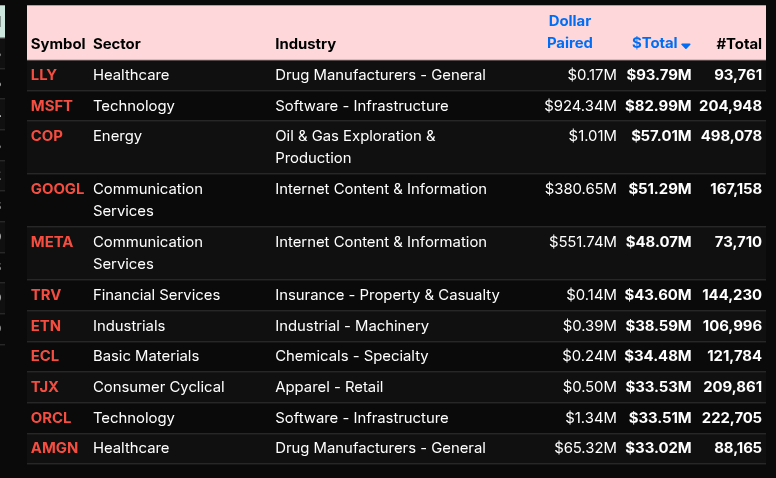

At the symbol level, the largest sell imbalances were concentrated in LLY, MSFT, COP, GOOGL, and META. On the buy side, NVDA led with over $408M paired, followed by AVGO, LRCX, MU, GS, JPM, GOOG, JNJ, XOM, and PLD. The strong presence of semiconductors and financials on the buy list reinforced the broader institutional bid that dominated most of the imbalance window before the final auction balanced out.

Technical Edge

Fair Values for March 11, 2026:

SP: 5.15

NQ: 24.25

Dow: 30.93

Daily Breadth Data 📊

For Tuesday, March 10, 2026

• NYSE Breadth: 43% Upside Volume

• Nasdaq Breadth: 56% Upside Volume

• Total Breadth: 51% Upside Volume

• NYSE Advance/Decline: 47% Advance

• Nasdaq Advance/Decline: 49% Advance

• Total Advance/Decline: 49% Advance

• NYSE New Highs/New Lows: 38 / 39

• Nasdaq New Highs/New Lows: 82 / 118

• NYSE TRIN: 1.18

• Nasdaq TRIN: 0.76

Weekly Breadth Data 📈

For the week ending Friday, March 6, 2026

• NYSE Breadth: 39% Upside Volume

• Nasdaq Breadth: 54% Upside Volume

• Total Breadth: 48% Upside Volume

• NYSE Advance/Decline: 26% Advance

• Nasdaq Advance/Decline: 32% Advance

• Total Advance/Decline: 40% Advance

• NYSE New Highs/New Lows: 320 / 160

• Nasdaq New Highs/New Lows: 318 / 550

• NYSE TRIN: 0.54

• Nasdaq TRIN: 0.39

ES & NQ Futures trading levels (Premium only)

NOTE DATE CHANGE #####

Trading Room Summaries

Polaris Trading Group Summary - Tuesday, March 10, 2026

The trading day began with overnight price action already achieving the upper 6820 target outlined in the Daily Trade Strategy briefing. The market opened on Cycle Day 1, with the Line in the Sand set at 6775, providing the key structural reference for the session.

Morning Session

Early market lean from David was neutral, suggesting opportunity on both sides of the trade ledger.

Bears initially held Command & Control with price trading below VWAP and the EMA cluster.

Sellers attempted to push the market lower toward the 6765 area.

Strong absorption appeared at 6765, signaling that buyers were stepping in aggressively.

Once price cleared the 6785 pivot, the structure shifted and bulls regained Command & Control.

This triggered a sharp upside reversal and momentum move higher.

Tick readings stayed elevated during the advance, confirming strong buying pressure.

The early reversal highlighted a key trading lesson:

Markets often shake traders out near extremes before making the real move.

Avoid the “shoulda, woulda, coulda” mindset and focus on structure and execution.

Midday / Cycle Objective

The bullish momentum continued once buyers took control.

Shallow pullbacks attracted additional buying interest, typical of Cycle Day 1 behavior.

Initiative buyers continued bidding price higher throughout the morning.

Price ultimately fulfilled the 3-Day Cycle target of 6841.63.

The target was achieved almost exactly to the tick, reinforcing the precision of the PTG cycle framework.

This move served as another example of:

Cycle Day 1 expansion after early absorption.

Level-to-level trading using the DTS framework.

Afternoon Trade Opportunity

Later in the afternoon, a high-probability D-Level setup developed.

A PTG trader executed a clean short entry directly at the D-Level.

The setup demonstrated textbook execution:

Precise entry at resistance.

Quick confirmation of rejection.

Cover lower as price reverted back toward the mid-VWAP zone.

David highlighted this as a “Triple-A Trade” and a perfect example of PTG level trading discipline.

Closing Action

During the final hour:

Price began showing signs of late-day weakness.

Momentum slowed as the session moved into the close.

The closing imbalance showed a $912M MOC Buy Imbalance.

Despite the late softness, the day had already completed its primary cycle objective earlier in the session.

Key Lessons from the Day

Absorption at key levels can signal major reversals (6765 defense).

Reclaiming pivots like 6785 often flips Command & Control quickly.

Cycle Day 1 commonly produces shallow pullbacks followed by expansion.

D-Level setups continue to provide high-quality trade opportunities.

Focus on structure and execution rather than missed trades.

Discovery Trading Group Room Preview – Wednesday, March 11, 2026

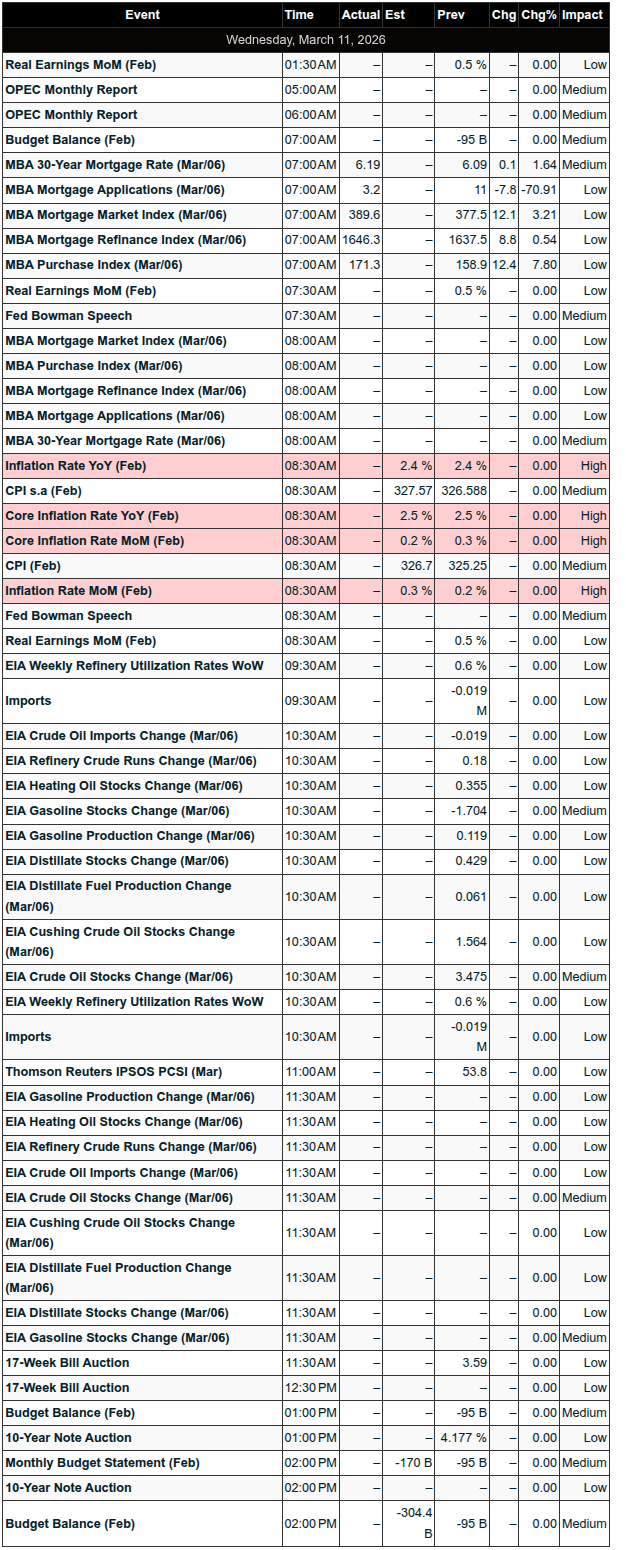

Macro Focus: Markets are watching the Middle East conflict, oil price volatility, and today’s CPI release at 8:30am ET.

Oil Market:

Oil prices are swinging after reports the IEA may propose a record strategic reserve release (potentially >182M barrels) to offset supply disruptions from the Iran war.

Confusion increased after incorrect comments from the U.S. Energy Secretary about a tanker escort in the Strait of Hormuz, later denied by the White House.

Diesel markets remain tight, with rising prices posing a larger economic risk than gasoline due to higher transportation and consumer costs.

Corporate News:

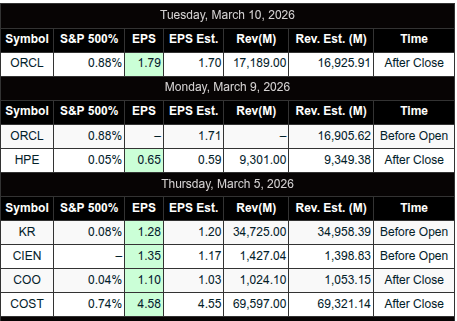

Oracle (ORCL): Shares jumped ~8% after beating earnings and raising 2027 revenue guidance to $90B, driven by AI data center expansion.

Nintendo: Shares rose over 10% following strong demand for the new Pokémon Pokopia game on Switch 2, which has sold out at major retailers.

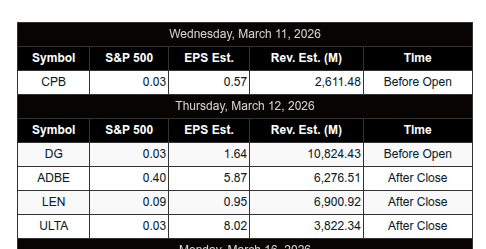

Earnings:

Premarket: HMY, KB

Thursday: Dollar General (DG), DICK’S Sporting Goods (DKS)

Economic Calendar:

8:30am ET: CPI + Fed Governor Bowman speaking

10:30am ET: Crude Oil Inventories

2:00pm ET: Federal Budget Balance

Market Structure / Volatility:

Volatility contracted Tuesday as oil eased.

ES 5-day average range remains elevated at ~141 points.

No clear whale bias overnight; large trader volume was light and mixed.

Technical Picture:

ES remains rangebound between 6600–7000 for ~6 months.

50-day MA: 6918 | 200-day MA: 6694, slowly converging.

A potential death cross in coming months could trigger bearish algo flows.

Despite geopolitical risks, the long consolidation suggests the eventual breakout bias may still be higher.

Key Levels:

Resistance: 6940–6935, 7230–7235

Support: 6560–6555