- The Opening Print

- Posts

- From Strait Fights to All-Time Highs — ES Traders Keep Hitting Bids Like Peace Is a Done Dea

From Strait Fights to All-Time Highs — ES Traders Keep Hitting Bids Like Peace Is a Done Dea

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

The Global Gas Gap: U.S. vs. The World

While the war in Iran has pushed U.S. gas prices to a four-year high of over $4 a gallon, American consumers still pay significantly less than their international counterparts. This discrepancy isn't due to the cost of crude oil, but rather domestic policy and production advantages.

Key Drivers of Lower U.S. Prices

The Tax Advantage: Taxes are the single biggest factor in price differences. In the U.S., federal and state taxes make up only about 15% ($0.60) of a $4 gallon, while in Europe, taxes typically account for 50% to 60% of the total retail price.

Energy Independence: As the world’s top oil producer, the U.S. is better shielded from global supply shocks than many other developed nations.

Infrastructure Strategy: While countries like Germany and France use high fuel taxes to fund public transit and green initiatives, the U.S. maintains lower rates to support its car-centric culture, where the average driver travels 13,000 miles annually.

Comparative Snapshot (March Averages)

Our View

The mullahs are out and the IRGC is in. Since early March, Brigadier General Ahmad Vahidi has consolidated power as Commander-in-Chief of the IRGC following a rapid succession of leadership due to the Iran war. Vahidi, a veteran hardliner, now functions as the "grey cardinal" of Tehran. By dominating strategic coordination and exercising a silent veto over civilian government, he has effectively become the most powerful man in the country, steering both the military machine and the political future of Iran. He's a hardliner and has shown no interest in negotiations with the US.

Wow, it's 8:19 pm Wednesday and the PitBull just called; while we were on the phone, crude oil jumped $4, and the ES dropped from 7162.50 down to 7105.50 and then rallied 40 points up to 7145.00 in less than 5 minutes off of some BS headline from the Washington Defender about some bogus headline on X. Just another bad example of how stupid things have gotten.

Guest Posts:

Dan @ GTC Traders

Running Her Hot ... Until Something Breaks

In the movie Ford vs. Ferrari (however true the actual incident was), it was shown that operating under the oderous committee’s of the Ford Motor Company ... the Ford GT has been ordered to keep it under 7000 RPM while racing. Preserve the engine. Stay within limits. Stay within what the engineers and the committees have deemed “safe.” And for a while … that constraint governed how the vehicle and driver raced. Speed was capped, and risk was managed. The system was contained.

Until Carroll Shelby had enough, finally breaks from that constraint … and sends a simple message to Ken Miles:

7,000 plus … Go Like Hell.

Push it beyond the limit. Run it hot. Accept that something may give … something may even break … but the decision has been made to win no matter what the cost.

That may bear some relevance to what we see in markets.

For a long time, we have stated that monetary policy has been far too loose for far too long. We have long complained that rates were cut too quickly, too aggressively. Financial conditions were eased into an environment that did not warrant it. The result was not stability … it was the embedding of structural inflationary pressure into the system we have discussed for years. We were right.

Then, for the last month and a half, we have witnessed crisis-level global energy dislocations. Physical shortages beginning to appear in oil and refined products from Europe to Asia. Major carriers cutting capacity as Lufthansa cut 20,000 flights, citing such shortages. Supply chains under stress.

And yet … U.S. equities push to new highs.

To many, this looked completely irrational. We’ll admit it was confusing to us for a while, before we realized that it is all part and parcel of the same policy environment.

As Danny Dayan correctly pointed out in referencing the Financial Conditions Index in his X stream ...

“When policy is restrictive, markets take even the smallest bad news poorly. When policy is loose, markets brush off even catastrophic news.”

That is exactly what we are witnessing.

The system has been told, implicitly and explicitly …

7,000 plus … Go Like Hell.

Liquidity is abundant. Risk is tolerated. Bad news is discounted. The marginal buyer is not focused on deteriorating fundamentals, but on the availability of capital and the expectation of continued accommodation. War? Ignored. Supply shock? Discounted. Structural inflation? Deferred.

Because the engine is being run hot.

And when you run a system hot for long enough … two things happen.

First, performance looks exceptional. Markets rally. Volatility compresses. Drawdowns are shallow. Participants begin to believe the system is more stable than it actually is.

Second … the underlying stress accumulates.

Components degrade. Margins for error shrink. Correlations tighten. Liquidity, which appears abundant, becomes conditional. And when the system finally reaches its limit … it does not fail linearly.

It fails all at once.

We have yet to see that last part. But we do feel that it is absolutely and consistently misunderstood. Loose financial conditions do not eliminate risk. They postpone its expression. They allow imbalances to build beneath the surface while price action signals the opposite.

Which brings us to the present.

Given the above we are not surprised by the rally. Given the policy backdrop, it is entirely consistent. In fact, it would be more surprising if markets were not rallying under these conditions.

But that does not make it sustainable.

Because the same factors driving the rally are the ones embedding the instability. Structural inflation is not resolved. Supply constraints are not resolved. Geopolitical tensions are not resolved. They are simply being overwhelmed … temporarily … by liquidity and positioning.

Run her hot.

Until something breaks.

We do not know the exact point of failure. No one does. Timing is always the variable that humbles participants. But we do understand the structure of the system we are operating in. And right now, that structure is one of excess, of compression, of latent instability.

So while others chase the highs, we remain grounded in process. Aware of the regime. Respectful of the asymmetry.

Because when the engine finally gives … it will not send a warning.

Until next time, stay safe and trade well.

Market Recap:

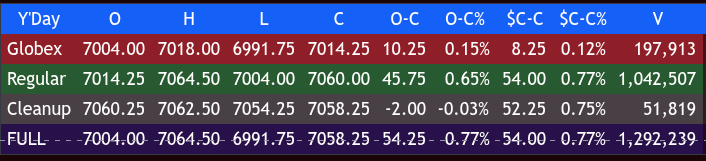

After a big whipsaw trade late in the day Tuesday, the ES traded up to 7157.25 and opened Wednesday's 9:30 ET regular session at 7150.75.

After the open, the ES traded up to 7166.25, pulled back to 7153.25, and rallied up to a lower high at 7165.75 at 10:40. It then sold off down to a new low at 7151.75 at 11:05, rallied up to 7164.00 at 11:25, and sold off down to a new low just below the VWAP at 7150.00 at 11:45.

The ES then back-and-filled above the VWAP in a 7 to 9 point range, broke down to a new low at 7146.50 at 12:25, and continued to back-and-fill just below and just above the VWAP. It traded 7146.75 at 12:55, rallied up to 7163.00 at 1:20, and fell back into another round of back-and-fill until 2:10, when the ES again pulled back under the VWAP down to 7150.50.

The ES traded up to 7159.50 at 2:45, had one last push under the VWAP down to 7150.00, and then stutter-stepped back up to 7165.75 at 3:55. It traded 7165.50 as the 3:50 cash imbalance showed $3.1 billion to buy, rallied up to 7173.00, and traded 7170.25 on the 4:00 cash close.

After 4:00, TSLA reported earnings and beat on earnings but missed on revenue; the ES sold off down to 7160.00 and settled at 7164.50, up 64.50 points or 0.91%. The NQ settled at 27,106.50, up 471.75 points or +1.77%, the YM settled at 49,888, up 149 points or +0.30%, and the RTY was up 15.80 points or +0.57% on the day.

In the end, you can read between the lines: all sorts of back-and-fill and low volume "thin to win," with $3.1 billion to buy on the close made for a NHOTC (new highs on the close). In terms of the ES's overall tone, it was firm and thin. In terms of the ES's overall trade, volume was the lowest in the last 9 sessions at 1.134 million contracts traded.

The CLK26 made a high at 93.73 and settled at 92.87, up 3.20 points or +x%; while still off its war highs. Gas prices remain stubbornly high but still lower than most places around the world.

Economic Calendar and Earnings

8:30 Initial jobless claims

9:45 S&P PMI

Earnings:

MCSA — Before Open

LUV — Before Open

CME — Before Open

INTC — After Close

DLR — After Close

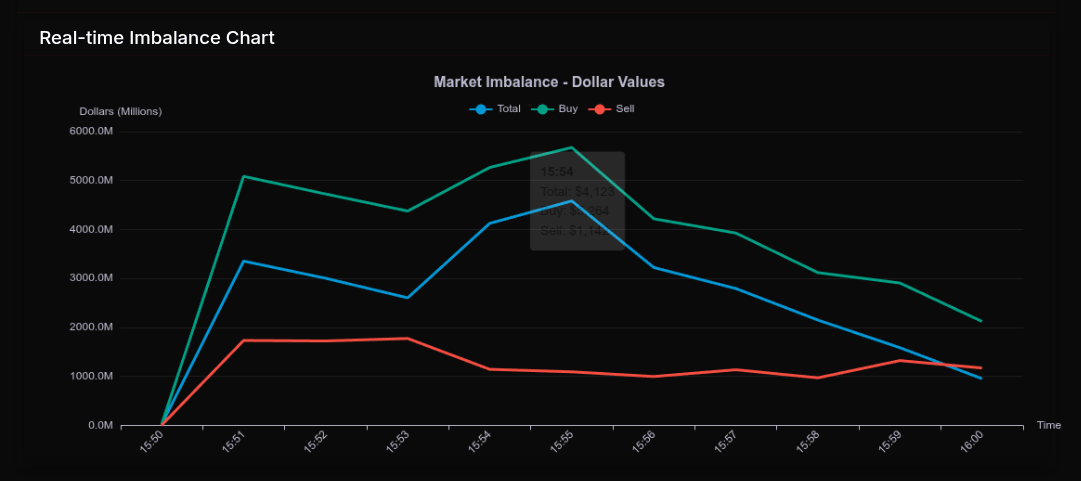

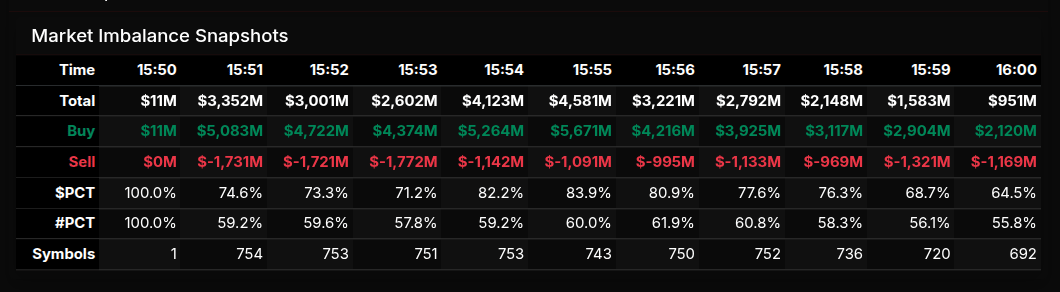

MiM

The MOC session opened with an immediate and aggressive buy-side imbalance, setting the tone early as capital flowed decisively into equities. At 15:50, the market showed a clean $2B buy imbalance, jumping to over $3.3B. From there, the session maintained strong buy control, peaking around 15:55 with total imbalances near $4.5B. The $PCT consistently held in the mid-70% to low-80% range, signaling persistent institutional demand rather than rotational noise.

As the session progressed into the final minutes, there was a gradual fade in total imbalance—from the $4B+ range down toward $951M into the close—but importantly, the buy-side dominance remained intact. Even at 16:00, the imbalance still leaned roughly +64.5%, showing that while participation thinned, directional conviction did not fully unwind.

Sector flows reinforced this strong buy-side narrative. Leadership came from Consumer Cyclical (+92.8%), Utilities (+91.5%), and Energy (+85.9%), all showing broad accumulation. Financials (+81.0%) and Communication Services (+74.5%) also contributed meaningfully, suggesting a risk-on posture across both defensive and growth areas. Technology printed a +66.8% lean, right at the threshold of trend, indicating strong but slightly more two-way participation relative to other sectors. The only notable outlier was Real Estate at -61.7%, reflecting a clear pocket of distribution.

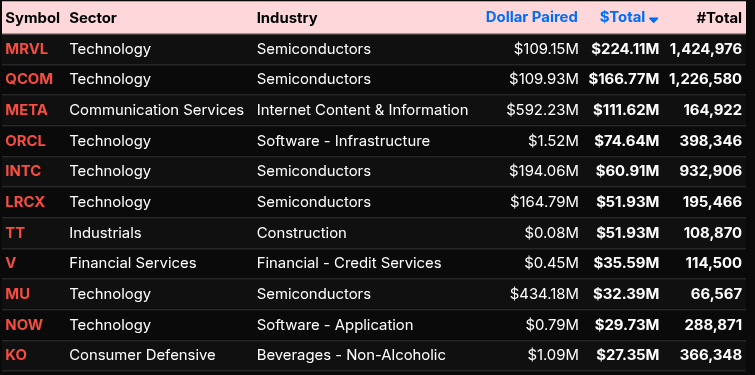

At the symbol level, flows were concentrated in mega-cap leadership. NVDA (+$461M), AMZN (+$331M), AVGO (+$222M), and TSLA (+$218M) led the buy programs, alongside strong participation in GOOG/GOOGL and MSFT. Semiconductors were particularly dominant, with names like MRVL, QCOM, INTC, and LRCX all seeing steady demand. META also stood out on the communication side, reinforcing the tech-heavy bid.

Overall, this was a structurally bullish MOC. The session opened with urgency, built into broad-based institutional buying, and while it tapered into the close, it never transitioned into meaningful sell pressure—indicating accumulation rather than rotation.

Replay:

Technical Edge

Fair Values for April 23, 2026

S&P: 34.09

NQ: 149.15

Dow: 170.43

Daily Breadth Data 📊

For Wednesday, April 22, 2026

• NYSE Breadth: 54% Upside Volume

• Nasdaq Breadth: 67% Upside Volume

• Total Breadth: 62% Upside Volume

• NYSE Advance/Decline: 55% Advance

• Nasdaq Advance/Decline: 64% Advance

• Total Advance/Decline: 60% Advance

• NYSE New Highs/New Lows: 106 / 15

• Nasdaq New Highs/New Lows: 279 / 76

• NYSE TRIN: 1.03

• Nasdaq TRIN: 0.88

Weekly Breadth Data 📈

For the Week Ending Friday, April 17, 2026

• NYSE Breadth: 66% Upside Volume

• Nasdaq Breadth: 73% Upside Volume

• Total Breadth: 70% Upside Volume

• NYSE Advance/Decline: 76% Advance

• Nasdaq Advance/Decline: 80% Advance

• Total Advance/Decline: 79% Advance

• NYSE New Highs/New Lows: 284 / 59

• Nasdaq New Highs/New Lows: 710 / 264

• NYSE TRIN: 1.70

• Nasdaq TRIN: 1.53

S&P 500/NQ 100 BTS Trading Levels (Premium Only)

BTS are daily generated levels created using a combination of proprietary calculations and AI to define an upper range target and a lower range target, split by a bull/bear line. You receive daily charts along with clear descriptions of each level to help guide your trading.

Take a Free Premium Trial to see them in action.

Today’s Economic Calendar

Earnings:

`

Trading Room News:

PTG Room Summary – For Wednesday, April 22, 2026

The day unfolded very much in line with the Daily Trade Strategy (DTS), with a strong emphasis on respecting key levels and staying aligned with the broader bias.

Pre-market & Plan

David set a clear tone early:

7125 was identified as the Line in the Sand (LIS) and held firmly overnight.

Bias was long above 7125, with a bull case targeting 7140 → 7145 → 7155.

The session was labeled Cycle Day 2, with expectations for typical rhythm and expansion.

Right out of the gate, the market validated the plan:

7155 target was fulfilled early, reinforcing the importance of trusting the pre-market roadmap.

Morning Session

The team maintained a “long-lean” posture, with David emphasizing that dips remained buyable.

Key execution concept: buying pullbacks into ATR support (ATR 7 Bull) and playing mean reversion setups.

Members discussed structure:

Watching consolidation breaks (CC) and first pullbacks

Staying aware of 50% retracement levels and prior key breakout zones (PKB)

Lesson: Structured pullbacks in a bullish environment provide high-probability entries—don’t chase, let price come to you.

Midday

As expected, edge diminished into midday:

Narrowing ranges

Choppy price action

David explicitly called out “midday chop” and advised stepping away.

Lesson: Recognizing when not to trade is just as valuable as finding entries. Protecting capital during low-edge periods is key.

Afternoon & Close

Market rotated tightly around mid-VWAP, confirming low momentum conditions.

Late-day development:

$3.1B MOC buy imbalance

Price pushed to close near highs of the day

This confirmed underlying strength and validated the earlier long bias.

Key Takeaways

Plan execution matters: The 7125 LIS and upside targets worked cleanly.

Stay aligned with bias: Long setups continued to offer opportunity throughout the morning.

Buy the dip in trend: ATR-based pullbacks were effective.

Avoid midday chop: Discipline in stepping aside preserved gains.

Closing strength reinforced that buyers controlled the session.

Overall, this was a clean, trend-respecting day where traders who trusted the levels, stayed patient on entries, and avoided overtrading likely had a solid session.

DTG Room Preview – Thursday, April 23, 2026

Macro / Geopolitics

U.S.–Iran negotiations stalled → weighing on equities & gold

Strait of Hormuz remains blocked → oil up 4th straight day

Ongoing geopolitical tension keeping volatility elevated

Earnings / Market Drivers

Corporate earnings helping offset macro pressure

Heavy earnings slate:

Premarket: AXP, BLK, CMCSA, HON, LMT, NEM, NEE, FCX, etc.

After close: Intel, SAP, GILD, BKR

Friday AM: PG, HCA, SLB, NSC

Tesla / AI / Robotics

TSLA beat earnings → initially higher, then reversed lower

Negative reaction driven by:

>$25B 2026 capex guidance

Implies continued negative free cash flow

Growth initiatives:

AI compute + new factories ramping

Megapack 3, Cybercab, Tesla Semi production prep

Robotaxi:

Miles nearly doubled QoQ

Cybercab expected to replace Model Y fleet

Optimus robots:

Factory prep starts Q2

V3 reveal expected mid-2026

Long-term goal:

Fremont: ~1M units/year

Texas: up to 10M units/year

Skepticism remains around real-world functionality

Semiconductors

Tesla to use Intel 14A process → major validation for Intel foundry business

Intel stock +3.6% ahead of earnings

TSMC:

New chip tech announced

Focus on lower cost + higher efficiency

Avoids need for expensive next-gen EUV machines

Economic Data (Today)

8:30am ET: Jobless Claims

9:45am ET: Flash PMIs

Volatility / Positioning

ES 5-day avg range: ~80 points (unchanged)

Whale bias: bearish into Jobless Claims

Overnight volume lighter than recent sessions

Technical Levels (ES)

Market still range-bound below ATH

Resistance:

7200–7203 (trendline)

7425–7430

Support:

7030–7035 (channel support)

6805–6810

6185–6180 (major downside)

Moving averages:

50D (6827) > 200D (6822) → bullish bias intact

Bottom Line

Market caught between:

Geopolitical risk (bearish)

Earnings + AI/semis momentum (supportive)

Focus today: Jobless Claims + key technical levels