- The Opening Print

- Posts

- Fed Is In The Air

Fed Is In The Air

Follow @MrTopStep on Twitter and please share if you find our work valuable!

FREE Two-Week Offer for the Opening Print Premium. Open up the Lean and other premium features for the next Two Weeks!

Our View

As far as I am concerned, it doesn't matter how you get from point A to B as long as you get there. Sometimes being right is skill, and sometimes it's luck — and other times it's a combination of both. I'm not sure how many times I spoke, posted, wrote, or livestreamed about the Stock Trader's Almanac stats showing the S&P being weak the week after the July expiration — and yesterday's decline was right on time.

After a slow start to the week during Monday's trade, Tuesday’s trade started in similar fashion with a 23.5-point range on Globex. Home Depot reported disappointing quarterly results and said it had shifted its stance on tariffs, saying modest price rises were now likely and that customers were holding off on larger home improvement projects. But it reaffirmed its annual guidance, and its stock rallied.

But it was not about Home Depot. It was about the weakness in the Magnificent Seven names, which lost $385 billion in market capitalization yesterday and now account for 34.2% of the S&P 500’s capitalization — more than one-third of the index.

I tried my best last Friday to debunk the Fed's efforts to lower interest rates 0.50% in September or 3 or 4 times by the end of 2025. What I think is, yesterday's selloff was a recalibration of interest rate expectations after the PPI and the ISM numbers showed a jump in inflation.

Everyone was plowing back into the big tech names that were already overbought, so it was somewhat of a reality check day. The big rotation was out of semiconductors, some AI names, and big tech.

In the end, I am not surprised at all by the weakness. In terms of the ES’s and NQ’s overall tone, every rally failed. The ES retreated 0.56%, closing near its lows on the day, and the NQ was down 1.6% — not exactly a kill job. In terms of the ES’s overall trade, volume was in line with recent figures, with 1.166 million contracts traded.

On the more positive side, S&P Global Ratings held the U.S.'s credit rating steady, saying revenue from tariffs would offset. The yield on the 10-yr note moved to 4.301%, the dollar made back some of its earlier losses with the dollar index closing up 0.1%, and Bitcoin sold off down to $13,200 after Treasury Secretary Scott Bessent said last week the U.S. doesn't plan to buy more assets for its bitcoin reserve. Gold fell 0.4%.

Our Lean — Danny’s Trade (Premium only)

Guest Posts — Polaris Trading Group

Prior Session was Cycle Day 2: This session’s rhythm went off the typical CD2 consolidation script, as price violated the 6455 – 6460 4-day support and broke lower.

Normally we would have seen the decline on CD1, which did not unfold, so we’ll note today as a “delayed decline.”

Member Ram P. won today’s KEWPIE Award with a timely observation of NAZ (@NQ) relative weakness, which spilled-over weighing on SPX (@ES) support breakdown. “Sharing is Caring” Thank you Ram 🙂

Range was 58 handles on 1.167M contracts exchanged.

For a more detailed recap of the trading session, click on this link: Trading Room RECAP 8.19.25

FREE TRIAL link to PTG/Taylor Three Day Cycle

…Transition from Cycle Day 2 to Cycle Day 3

Transition into Cycle Day 3: Prior decline flushed down fulfilling the 6421.50 CD2 Projected Range decline, (screenshot) as noted in PTG’s Live Trading Room.

Price is currently below the CD1 Low (6456) and based on historical averages there is a 91.43% chance of reclaiming the CD1 Low.

However after that is reached then anything goes.

Of course, nothing changes for PTG…Simply follow your plan. Take only Triple A setups and manage the $risk. ALWAYS HAVE HARD STOP-LOSSES in-place on the exchange.

PTG’s Primary Directive (PD) is to ALWAYS STAY IN ALIGNMENT with the DOMINANT FORCE.

As such, scenarios to consider for today’s trading.

Bull Scenario: Price sustains a bid above 6430+-, initially targets 6445 – 6450 zone.

Bear Scenario: Price sustains an offer below 6430+-, initially targets 6415 – 6405 zone.

PVA High Edge = 6458 PVA Low Edge = 6421 Prior POC = 6425

ESU

Thanks for reading, PTGDavid

MiM and Daily Recap

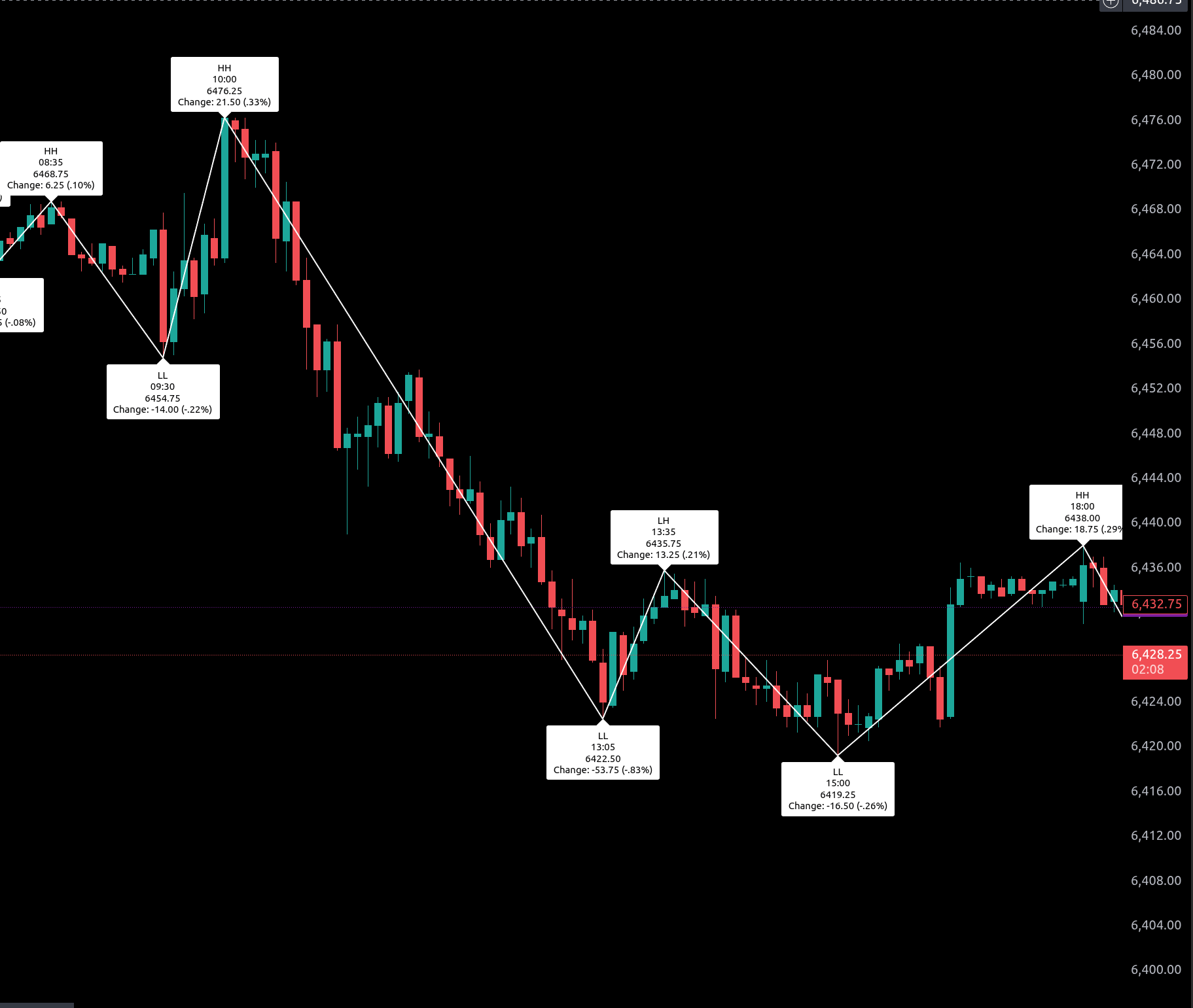

The overnight Globex session opened at 6468.50 and struggled to sustain early strength. After reaching a high of 6477.50 at 18:00, ES reversed lower and fell steadily, marking successive declines into the late evening. The first low came at 23:10, printing 6459.50, before a minor bounce to 6466.00 at 23:20. Selling pressure persisted, driving prices to the Globex session low of 6454.00 at 01:40, a 23.50-point decline from the evening high. Buyers briefly regained traction, lifting ES to 6469.00 at 05:20, but the move was capped. Another rally attempt peaked at 6468.75 by 08:30, only to fade into fresh weakness at 09:30. The session settled at 6466.25, down 2.25 points (-0.03%) from the prior close.

The cash session opened at 6466.25 and quickly tested resistance, spiking to 6476.25 at 10:00, its intraday high and a 47.5-point gain from the Globex low. However, momentum reversed sharply, with sellers pressing ES to 6420.50, marking the day’s low and a 55.75-point slide from the cash high. An afternoon rebound carried ES back to 6435.75 at 13:55 and then to 6438.00 by 16:00, but the recovery lacked conviction. The regular session closed at 6432.75, down 33.50 points (-0.52%) from the open and off 36.00 points (-0.56%) versus the prior cash settlement.

The cleanup session saw a mild bid, with futures lifting from 6432.50 to settle at 6435.00, a small gain of 2.25 points (+0.03%). Full-session volume reached 1,167,168 contracts, with 1,023,556 traded during the regular session, reflecting healthy liquidity.

Market Tone & Notable Factors

Overall tone was bearish, as intraday rallies were met with steady selling, producing lower highs and a firm downward bias. The Globex trade was choppy but held in a narrow range, while the cash session featured more decisive downside momentum, highlighted by a mid-day flush to 6420.50.

Despite late-session stabilization, buyers could not offset the weight of earlier losses, leaving ES lower on both an open-to-close and close-to-close basis. The $C–C change of -36.00 points (-0.56%) reinforced the downside tone.

The Market-on-Close imbalance data showed $1.17B in total notional flow, with 62.9% on the buy side but only 51.4% of symbols participating. While the dollar imbalance leaned positive, it failed to trigger a strong lift into the bell, suggesting that institutional buyers were selective and concentrated rather than broad-based. This imbalance offered only modest support and was not enough to change the day’s directional outcome.

In summary, Tuesday’s action reflected heavy intraday distribution, with sellers in control despite occasional countertrend rallies. The inability to hold rebounds underscores a cautious tone heading into the next session, with bears still pressing their advantage.

Technical Edge

Fair Values for August 20, 2025:

SP: 18.53

NQ: 76.02

Dow: 69.39

Daily Market Recap 📊

For Tuesday, August 19, 2025

• NYSE Breadth: 50% Upside Volume

• Nasdaq Breadth: 40% Upside Volume

• Total Breadth: 41% Upside Volume

• NYSE Advance/Decline: 56% Advance

• Nasdaq Advance/Decline: 35% Advance

• Total Advance/Decline: 43% Advance

• NYSE New Highs/New Lows: 67 / 21

• Nasdaq New Highs/New Lows: 116 / 102

• NYSE TRIN: 1.54

• Nasdaq TRIN: 0.81

Weekly Market 📈

For the week ending Friday, August 15, 2025

• NYSE Breadth: 55% Upside Volume

• Nasdaq Breadth: 63% Upside Volume

• Total Breadth: 60% Upside Volume

• NYSE Advance/Decline: 65% Advance

• Nasdaq Advance/Decline: 65% Advance

• Total Advance/Decline: 59% Advance

• NYSE New Highs/New Lows: 267 / 94

• Nasdaq New Highs/New Lows: 571 / 303

• NYSE TRIN: 1.44

• Nasdaq TRIN: 1.09

ES & NQ Futures trading levels (Premium only)

Calendars

Economic

Today

Important Upcoming / Recent

Earnings

Upcoming

Recent

Trading Room Summaries

Polaris Trading Group Summary - Tuesday, August 19, 2025

Opening & Pre-Market

David started the day with links to resources, strategy tools, and the CFTC disclaimer.

Trader quote of the day focused on discipline: controlling orders, not outcomes.

Early concern about low volatility and limited price action carried over from the previous few sessions.

David forecasted a high chance of market "fukery" due to lack of rhythm.

Manny and others noted risk of another sub-30-point range day.

Market Open & Morning Session

Volume and rhythm remained low through the open.

Traders discussed broad sector rotation, with Ram noting a shift into defensive sectors like healthcare.

A quick “dip and rip” pattern appeared, with price action stuck between SPX gamma levels (6440–6450).

Ram received recognition for a good read on sector rotation.

Key Setups and Trade Execution

Internals began turning bullish mid-morning with rising breadth and VIX pulling back.

David confirmed a potential discount long setup being watched. Roy and others engaged, but it didn’t fully play out.

Discussion around RSPR and manual pivot points highlighted a learning moment about trade plan criteria and setup confirmation.

Semiconductor weakness observed by Tom Bear, with Nvidia notably down 1.8 percent.

Price tagged the 6455–6450 zone, aligning with David’s bear scenario trigger.

Main Trade of the Day

David called out the @NQ Open Range Short setup.

Targets were methodically hit throughout the session.

By 1:45 PM, David confirmed all targets were fulfilled on the short.

Cycle Day 2 violation target (6427) and projected low (6421.50) were both fulfilled later in the afternoon.

This price action followed David’s note from the previous DTS, which warned of a downside test of balance.

Trade Lessons & Analysis

The failed discount long was referenced as the "Barbara Lopez Trade" (BLT), turning into a humorous but valuable lesson about invalidated setups.

Traders discussed strategy around A10 bounces and how often they tend to hold.

Ram preferred the manual RSPR approach, reinforcing discretionary trading value in certain conditions.

David shared insight into how CD1 and CD2 structure plays into price discovery and failure of balance support.

Late Session

Afternoon chop around fib clusters observed by Manny, with some muted reactions near T4 money box.

MOC Buy Imbalance of $976M noted late in the day.

Close

David wrapped up by saying, “Taco Tuesday served up a burrito,” summarizing the surprise activity and productivity of the day.

Despite a slow start, the session delivered a clean directional short with technical precision.

Traders were reminded of the value of waiting for structure and letting setups come to them.

Discovery Trading Group Room Preview – Wednesday, August 20, 2025

Tech Weakness: US tech stocks fell sharply, led by declines in Palantir (PLTR) and Nvidia (NVDA). Semiconductor names also under pressure after reports the US may seek equity stakes in CHIPS Act-funded companies; Micron (MU) down 2% premarket.

Apple Alert: iPhone sales in China fell 31.3% YoY in June, contributing to a 9.3% drop in overall phone sales.

Earnings Focus: Key reports this morning from Target (TGT), TJX (TJX), Lowe’s (LOW), ADI, FUTU, HTHT, EL, and SNPS. NDSN reports after the bell.

Macro Watch: July FOMC Minutes release at 2:00pm ET, with Fed speakers Waller (11:00am) and Bostic (3:00pm). Crude Oil Inventories drop at 10:30am ET.

Oil Flows: India trims Russian oil imports under US pressure; China picks up the slack with cheaper cargoes.

JHX Warning: James Hardie (JHX) plunges 28% after earnings; company cites weak US housing demand and deferrals in remodeling.

Market Setup: Volatility is compressing with ES ADR at 43.50. Whale bias bearish into US open. ES broke short-term trend support; next key support seen at 5362/65. Resistance at 6617/22, 6646/51.